Introduction

The big tech cash hoarding : a symptom of a insufficiently competitive environment

From the symptoms to the cause

Market power and anticompetitive practices

Are the tech giants natural monopolies?

Astrong antitrust policy and a new regulatory framework to foster competion and innovation

Adapting antitrust legislation to the realities of the digital economy

Tougher enforcement of competition law

Beyond antitrust: the need for new regulations

General conclusion and recommandations

Appendices

References

b. A trend for concentration.

A second symptom of reduced competitive intensity can be seen in the trend for consolidation that has prevailed within the sector for a decade.

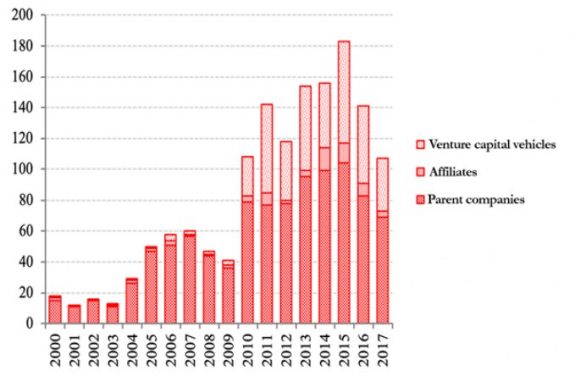

Indeed, it is apparent that the tech giants’ remarkable success over the past twenty years has been combined with multiple acquisitions of relatively young companies. An analysis of data extracted from the Mergermarket specialist platform reveals significant acquisition activity among the big tech companies, which has intensified since the end of the 2010s (see Graph 1).

Graph 1: Acquisitions and minority investments by acquirer type – Top 10 Tech US (number of deals)

© Fondation pour l’innovation politique, November 2018

Acquisitions. We will firstly consider acquisitions resulting in takeovers of third-party companies by any of the big tech firms.

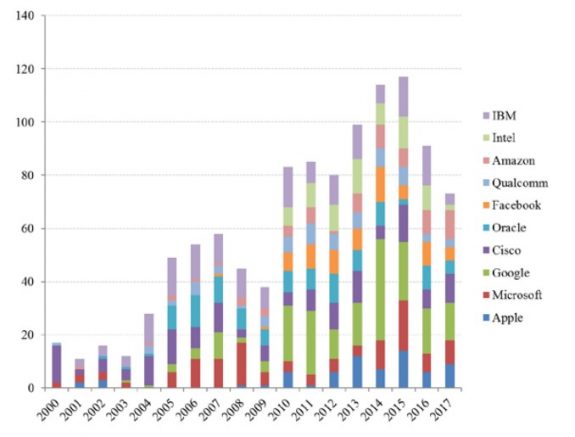

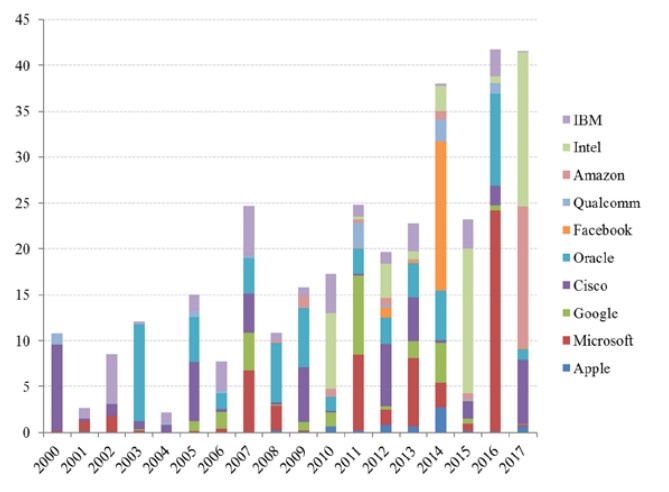

As indicated in graph 2 below, all the tech giants without exception have contributed to the process of consolidating the sector – each of them has performed over ten acquisitions on average per year since the start of the decade. A closer examination of these transactions reveals that the tech giants very frequently acquire new companies operating in similar or adjacent markets to their own (see Tables 2(a) and 2(b) in the appendices). This model was initiated by Google with the acquisitions of YouTube (2006) and Android (2007), followed by Amazon with Zappos (2009), Quidsi (2010) and Souq (2017), and Facebook with Instagram (2012) and To Be Honest (2017). Such consolidation also occurs at later stages in target companies’ development. Examples of this include the acquisition of WhatsApp by Facebook in 2014, Tandberg by Cisco in 2009, Skype and LinkedIn by Microsoft in 2011 and 2016 and Beats by Apple in 2014. The curve showing the sums invested in acquisitions shows that this phenomenon has gained momentum in recent years (see graph below). Whether in terms of ‘small’, strategic acquisitions or takeovers of more mature companies, the same observation applies: the tech industry is in the grip of increasing horizontal consolidation2.

Graph 1: Acquisitions and minority investments by acquirer type – Top 10 Tech US (number of deals)

© Fondation pour l’innovation politique, November 2018

Graph 3: Acquisitions by parent companies and affiliates in billions of dollars (US)

Copyright :

© Fondation pour l’innovation politique, November 2018

Venture investments

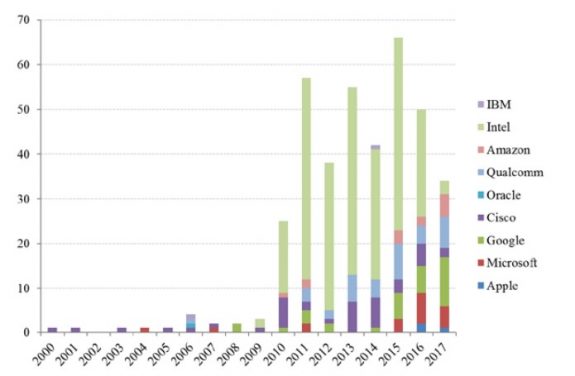

In addition to these takeovers, they also make minority investments mostly through their internal venture capital vehicles3. As the graph below shows, these are very frequent and their momentum increased considerably at the start of the last decade. We believe that this process is part of big tech companies’ efforts to monitor technological innovations. Anxious not to repeat their predecessors’ mistakes4, they secure special access to innovation through these investments. Consequently, they are able to closely monitor the emergence of any promising new technology from the earliest stages.

Graph 4: Minority investments by in-house venture capital vehicles (number of deals)

©Fondation pour l’innovation politique, November 2018

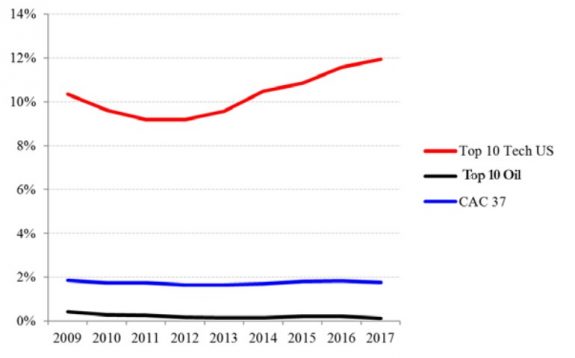

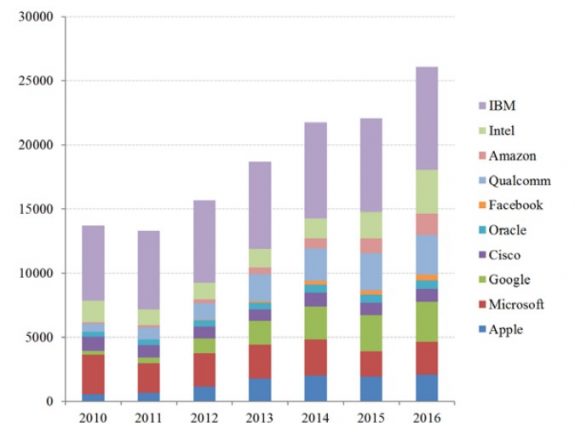

These venture investments supplement internal R&D work, which is carried out on a colossal scale. Indeed, the tech giants’ R&D spending ratios are five to six times higher than those of traditional industries (see the graph below). The strategy employed here is the same as that used to guide external investments: while allocating part of their R&D to their core business, the big tech companies also run research departments focused on completely new verticals. Examples include the Google X laboratory that notably worked on driverless cars (Waymo) and augmented reality (Google Glass) and Facebook’s defunct Aquila project aimed at developing a solar-powered drone.

Graph 5: Comparison of R&D expenditure in percentage of revenues

© Fondation pour l’innovation politique, November 2018

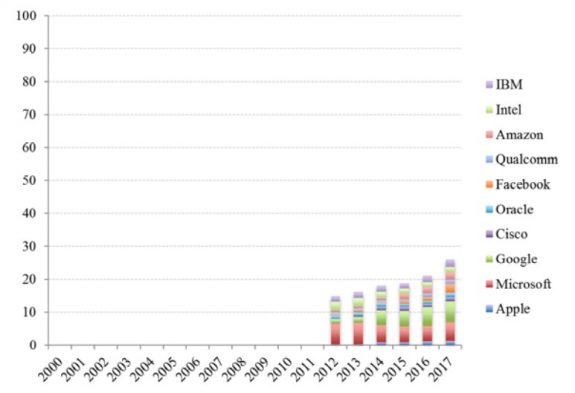

We note that most big tech lobbying takes place in the United States: expenditure on lobbying European institutions is substantially lower. This may be due to the fact that the economic stakes are higher for them in the United States than in Europe. It may also be because the scope of the European authorities’ powers is narrower than that of the US authorities, given the prerogatives retained by member states in the EU. Finally, this discrepancy may be down to greater permissiveness shown by the US authorities toward the big tech firms, with a view to protecting US strategic interests.

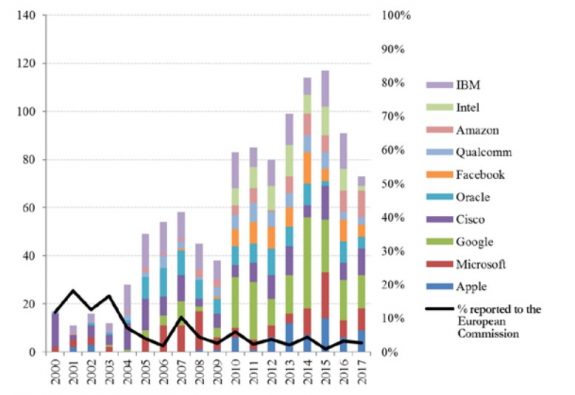

Graph 6: Expenditure on lobbying US institutions in millions of dollars (US)

© Fondation pour l’innovation politique, November 2018

Undoubtedly, the tech giants have opted not to repeat Microsoft’s mistake of having little presence in Washington in the early 1990s when its troubles with the antitrust authorities began. We should finally note that the big tech firm’s influence in the political arena exceeds their lobbying capacity. Their direct access to the majority of citizens gives them considerable means of applying pressure. For instance, in 2012, during discussions on the ‘Stop Online Piracy Act’ and ‘Protect IP Act’ bills in Congress, Google added a black banner to its search engine condemning the ‘censorship’ that was about to be imposed on it.

Graph 7: Expenditure on lobbying European institutions in millions of dollars (US)

©Fondation pour l’innovation politique, November 2018

a. Mergers and acquisitions

Although Europe appears to be gradually realizing just how important increased monitoring of big tech abuses of dominant position is, it seems to have made much less progress on examining mergers and acquisitions in the tech sector.

Reviewing thresholds for reporting mergers and acquisitions

In evidence of this, Tables 2(a) and 2(b) in the appendices reveal a striking fact – most strategic acquisitions performed by the big tech firms are not even examined by the European Commission. Why is this the case? These mergers and acquisitions are not notified to the European authority as they do not meet threshold criteria for reporting. The graph below shows a clear downward trend in the percentage of deals reported to the European Commission since the early 2000s.

Graph 8: Identified mergers and acquisitions versus those reported to the European Commission (number of deals)

© Fondation pour l’innovation politique, November 2018

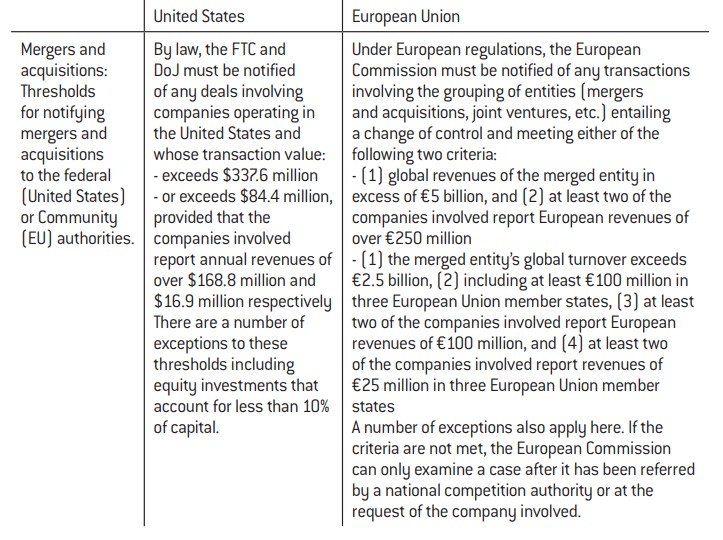

Table 1: Notification thresholds for mergers and acquisitions (United States and European Union)

Copyright :

© Fondation pour l’innovation politique, November 2018

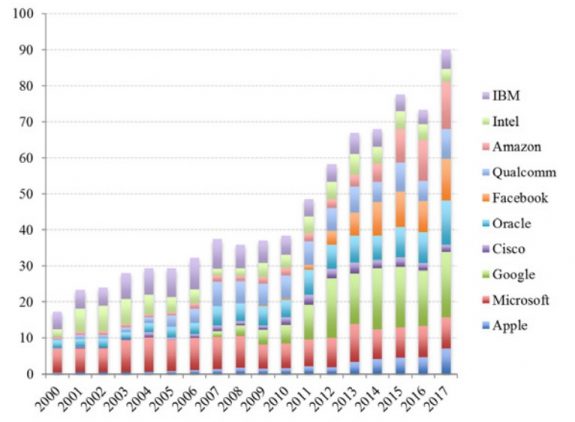

One key observation should be made. A patent war is currently raging among the big tech firms and, more generally, in the tech industry. Apple, Microsoft, Intel, Google, IBM and Qualcomm were each granted rights to over two thousand patents in 2017. The graph below illustrates a clear upward trend for the number of patents filed annually.

There has been a clear rise in the number of patents used to protect companies from attacks or as legal weapons. Armies of lawyers have joined engineers in R&D departments in an attempt to patent any potentially innovative idea in a move that is both defensive and offensive in nature. Consider the following statistic provided by one observer 46: between 2010 and 2012, $20 billion was spent in the United States on legal battles concerning patents in the smartphone market alone.

Graph 9: Patents filed by parent companies in the United States (in numbers per year)

©Fondation pour l’innovation politique, November 2018

Source : U.S. Patent and Trademark Office.

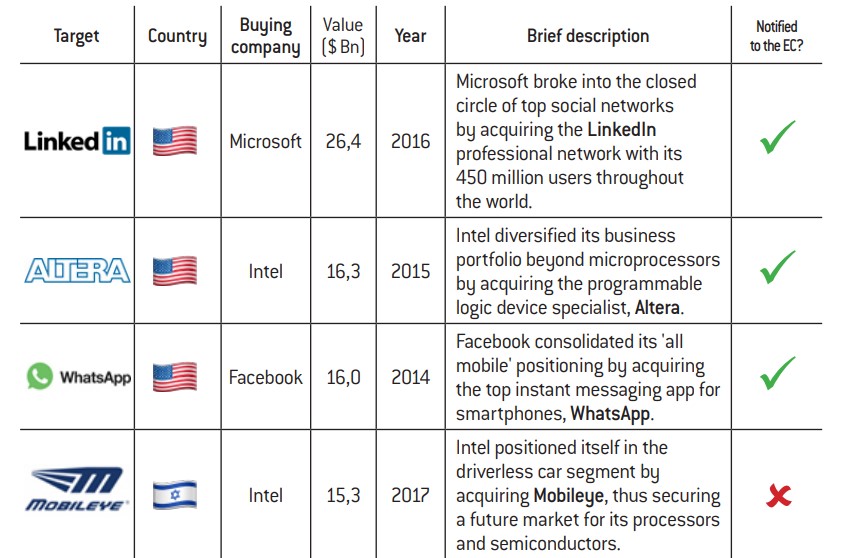

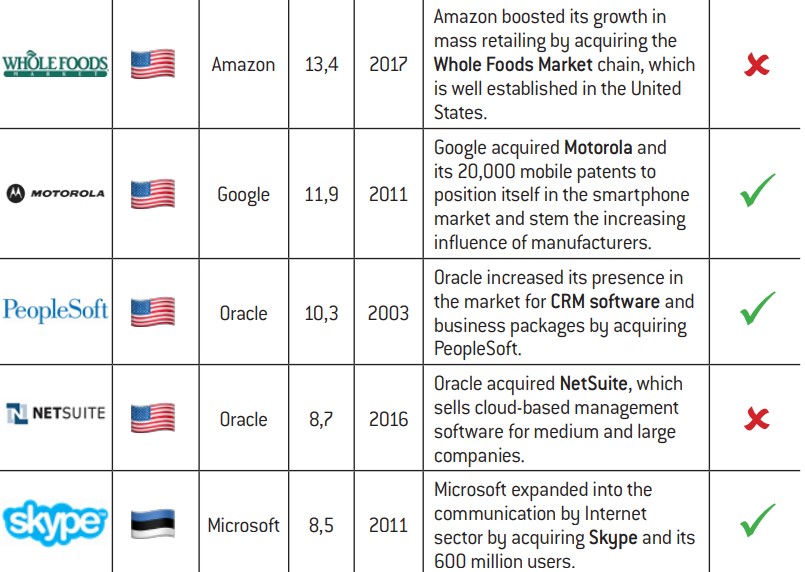

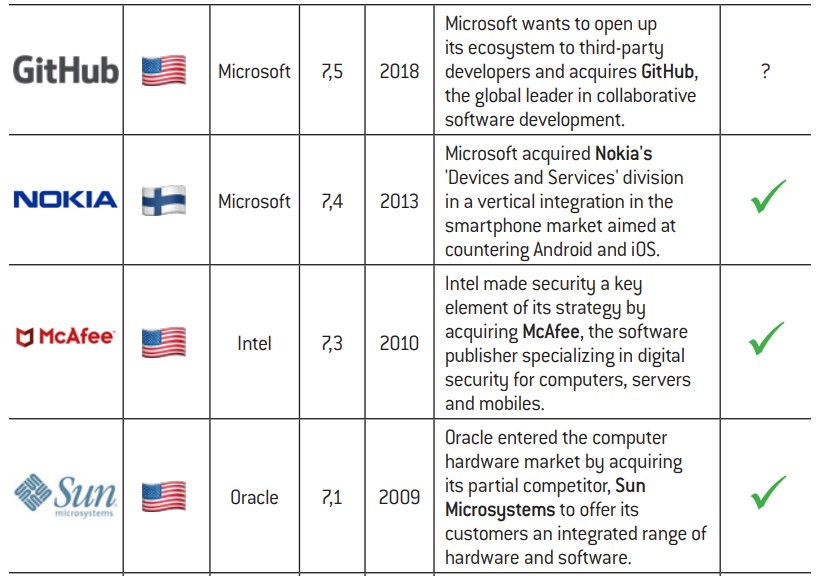

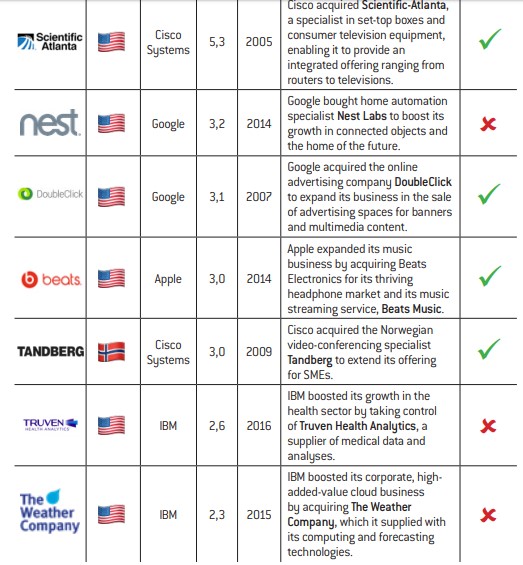

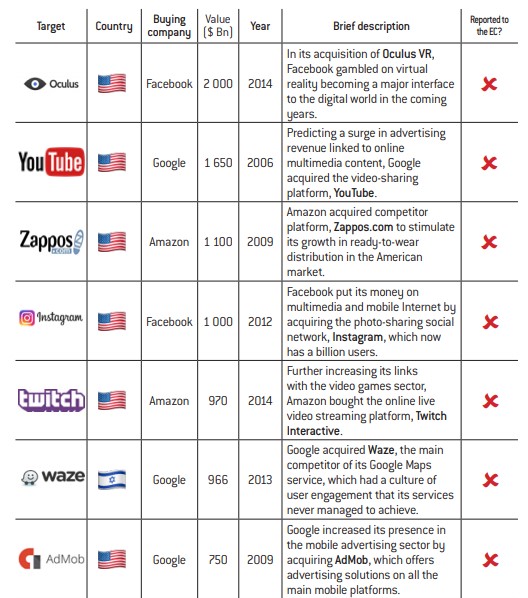

Appendix 2(a) Key acquisitions:

A selection of 20 major acquisitions of a value exceeding $2 billion performed by the big tech companies since 2000.

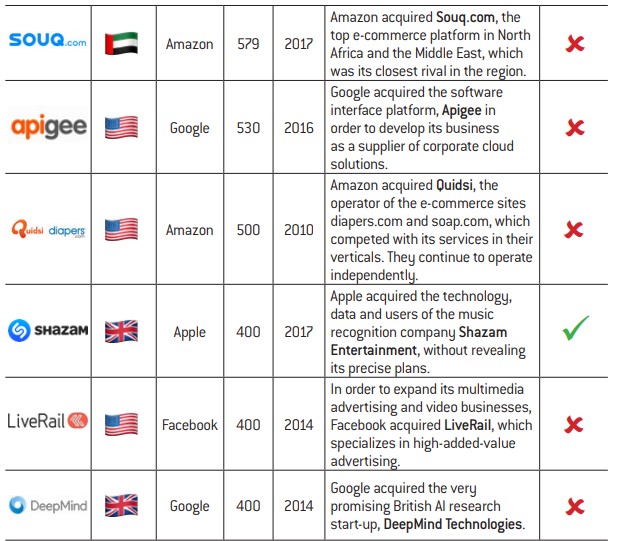

Appendix 2(b) Strategic acquisitions:

A selection of 20 major acquisitions valued under $2 billion that have been performed by the big tech companies since 2000.

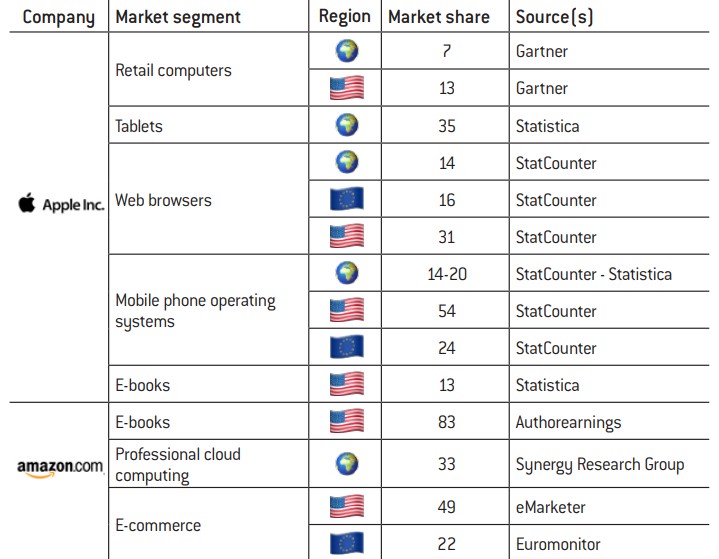

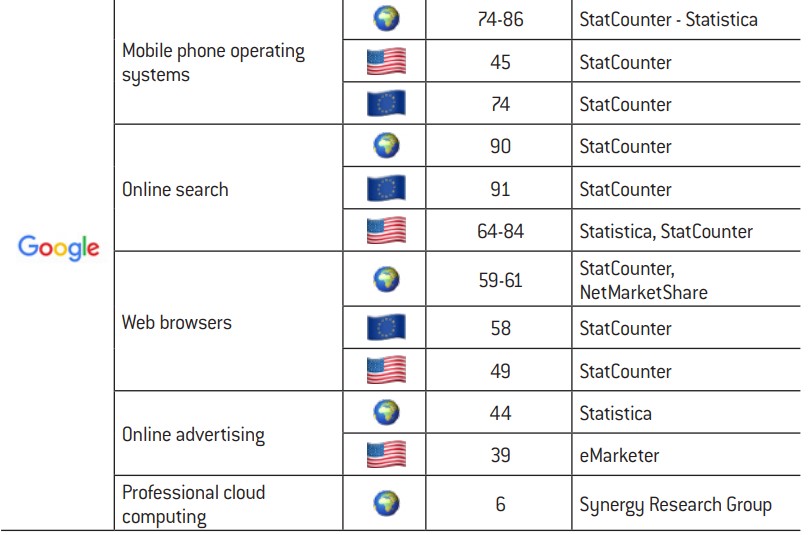

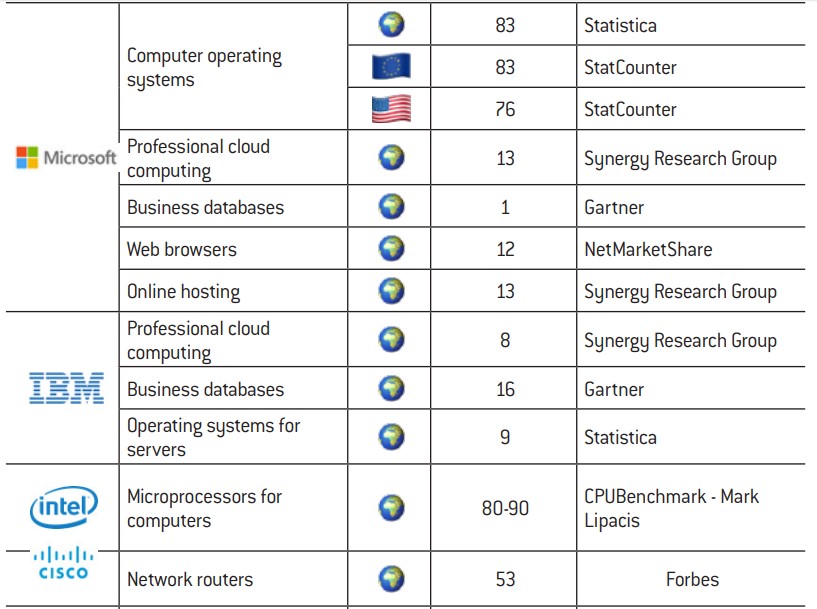

Appendix 2(c) Big tech market shares:

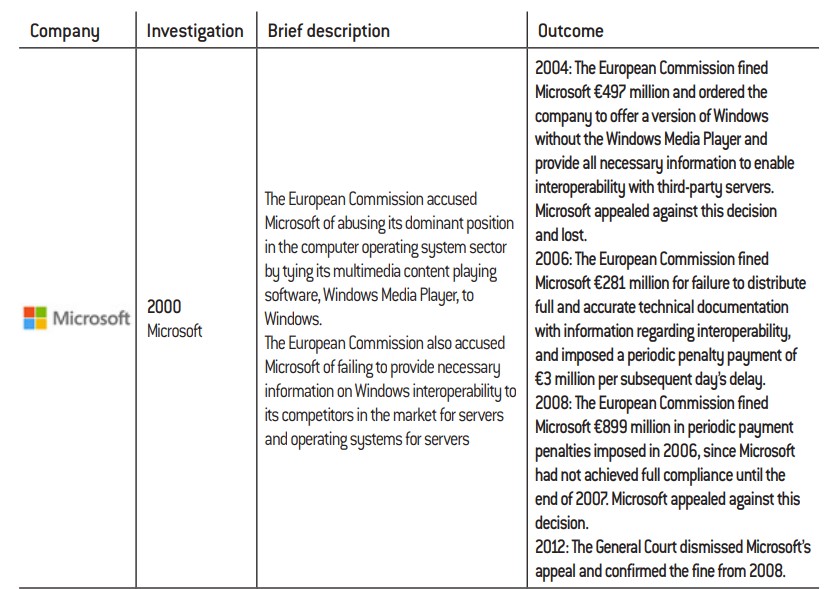

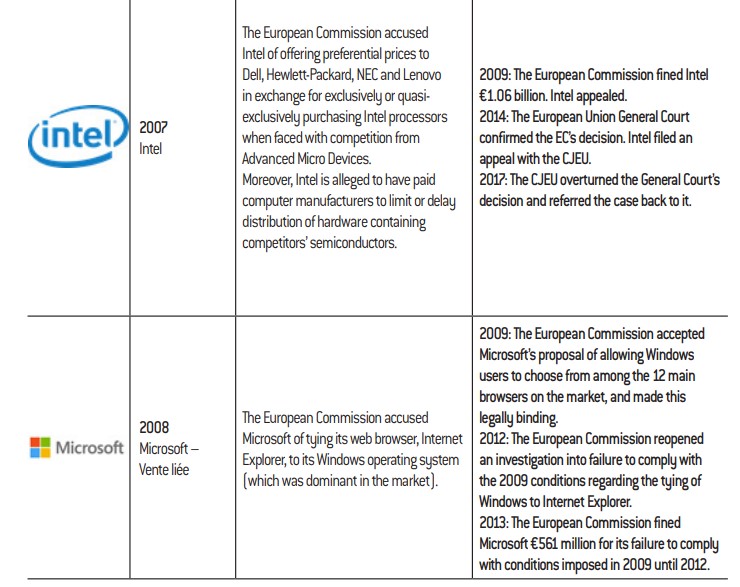

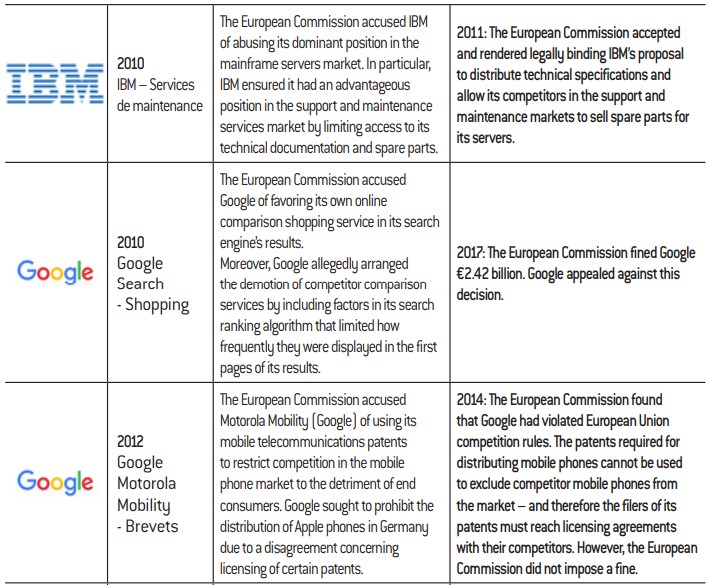

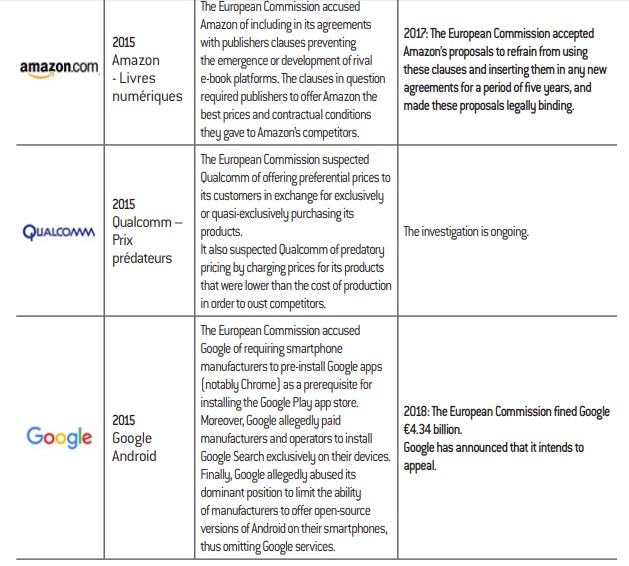

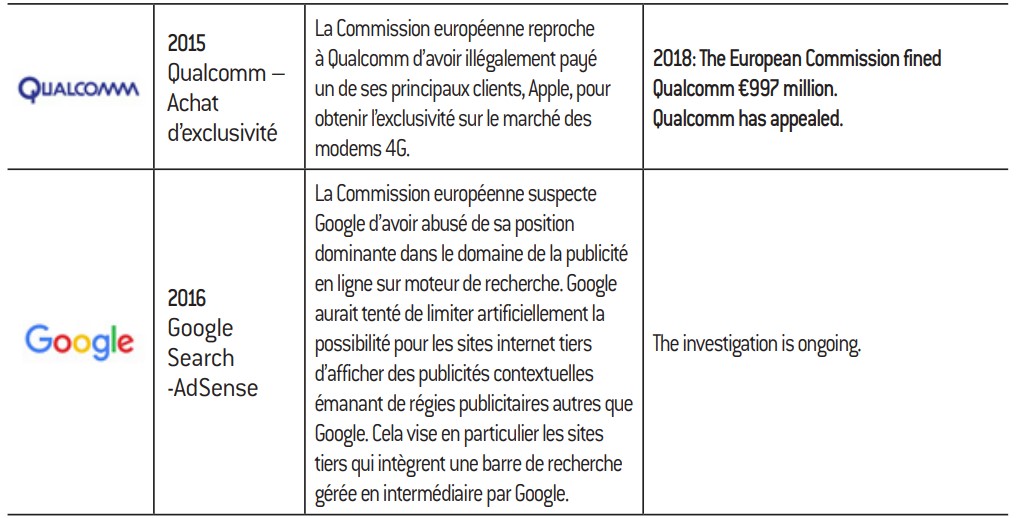

Appendix 2(e) Key cases of abuse of dominant position involving the big tech firms in Europe since 2000:

Appendix 2(f) Key big tech mergers and acquisitions since 2000:

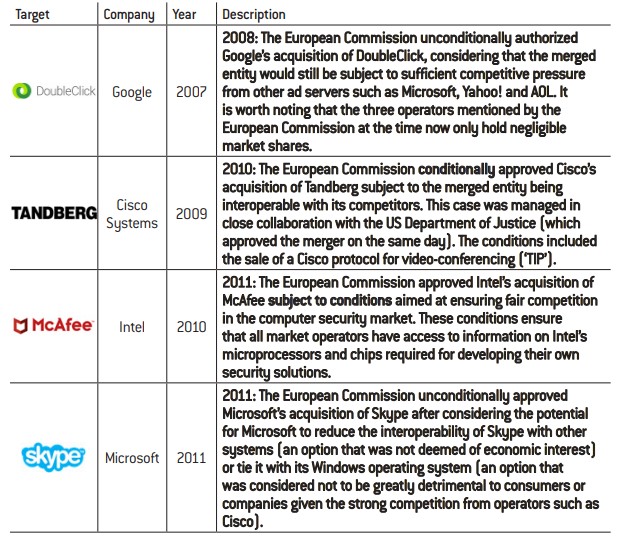

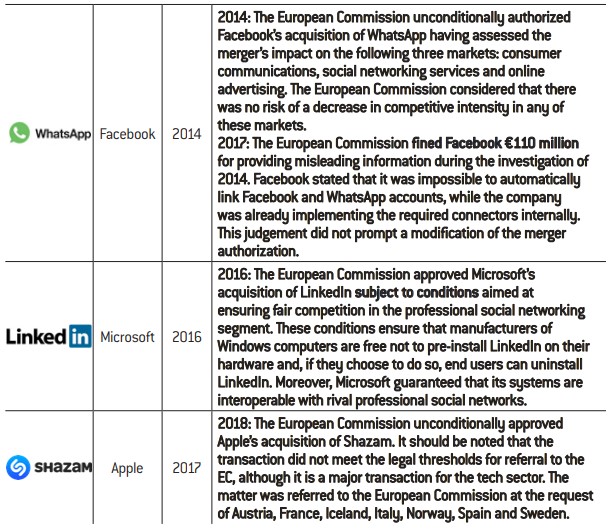

A selection of mergers and acquisitions that have been conditionally authorized by the European Commission or are of specific interest due to their strategic significance.

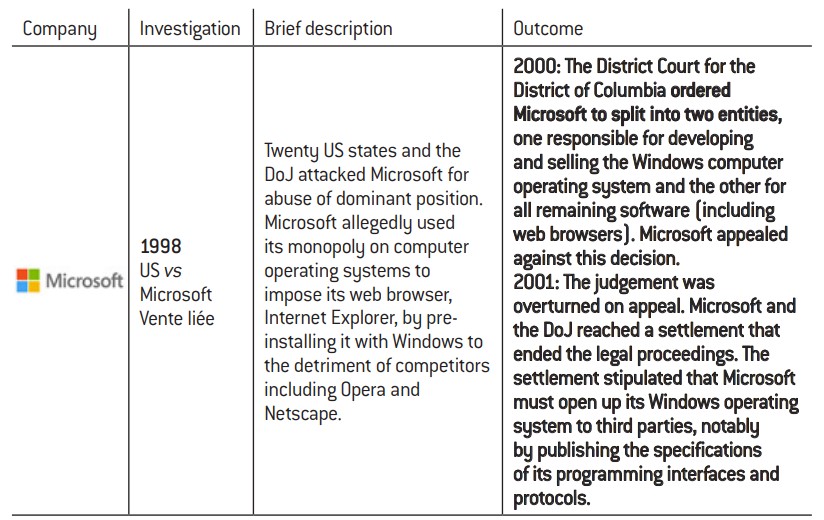

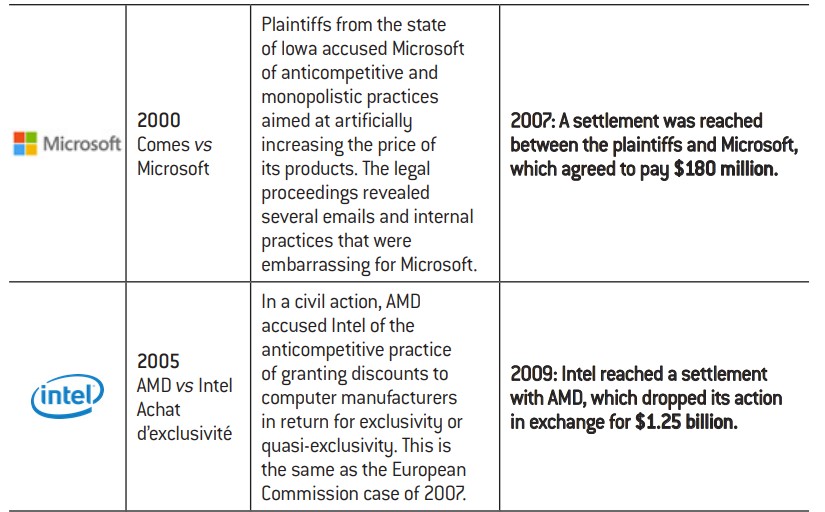

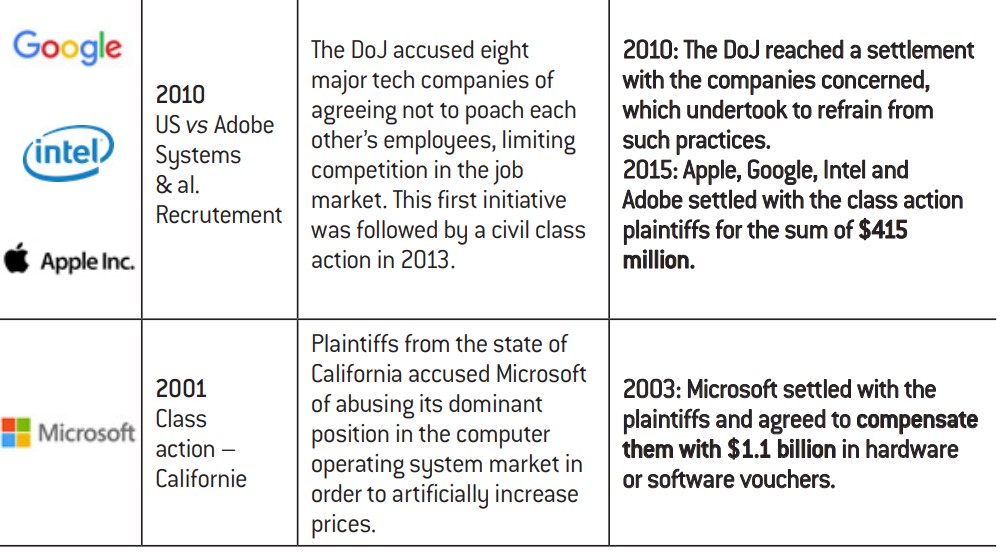

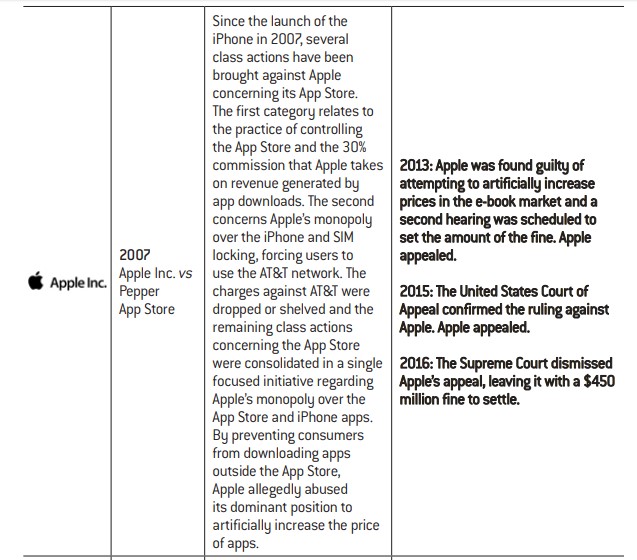

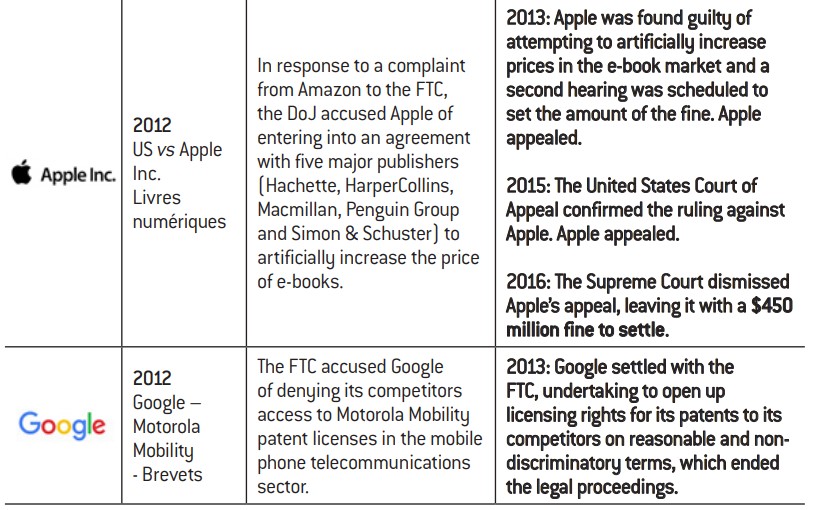

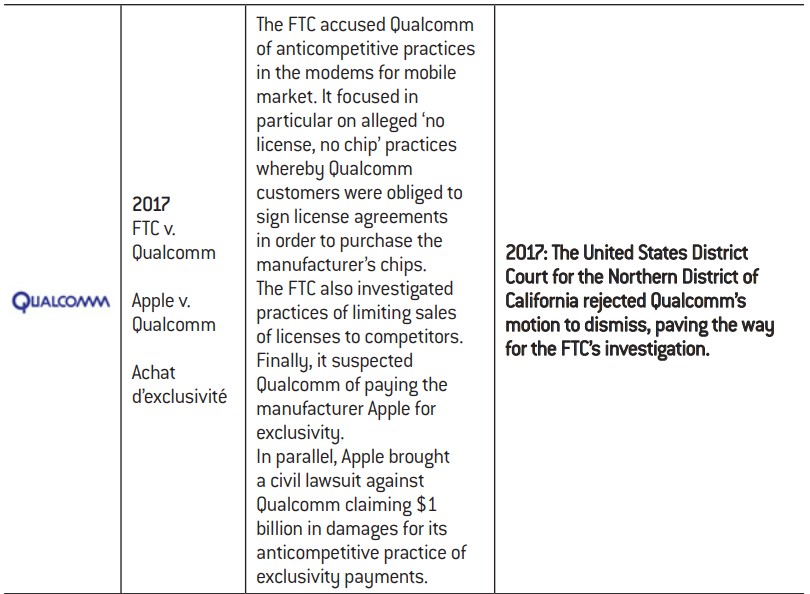

Appendix 2(g) Key big tech antitrust cases in the United States since 2000:

No comments.