Europe in the face of American and Chinese economic nationalisms (2)

Foreign anti-competitive practices

The multilateral framework of the world trade organization (WTO)

A historically divided Europe on trade defence

Moderate use of anti-dumping and anti-subsidy instruments

The regulatory and institutional specificities of European trade defence

Appendices

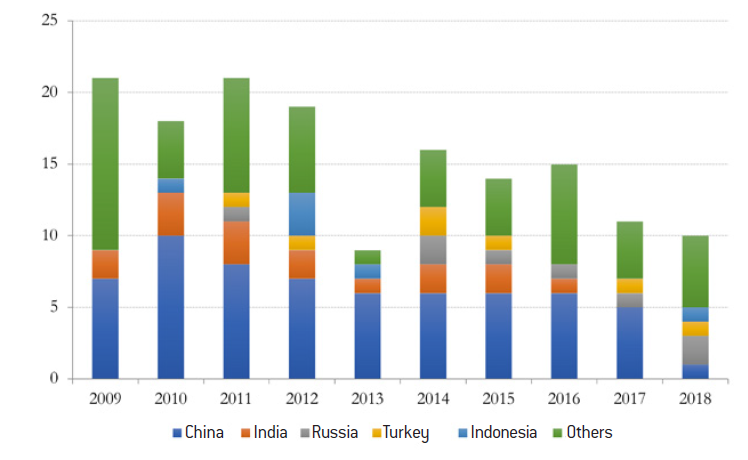

Geographical targets for defence instruments, in number of measures in force at the end of 201

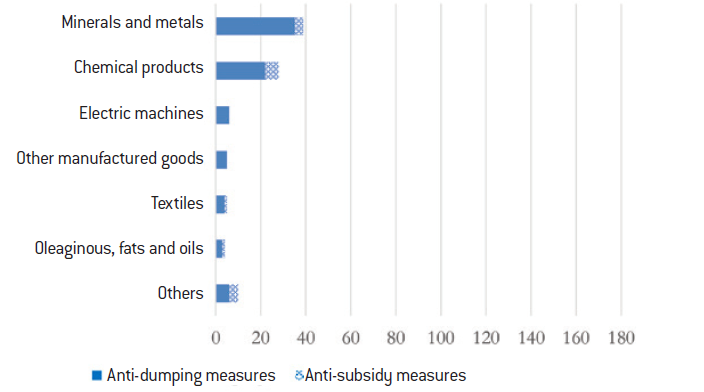

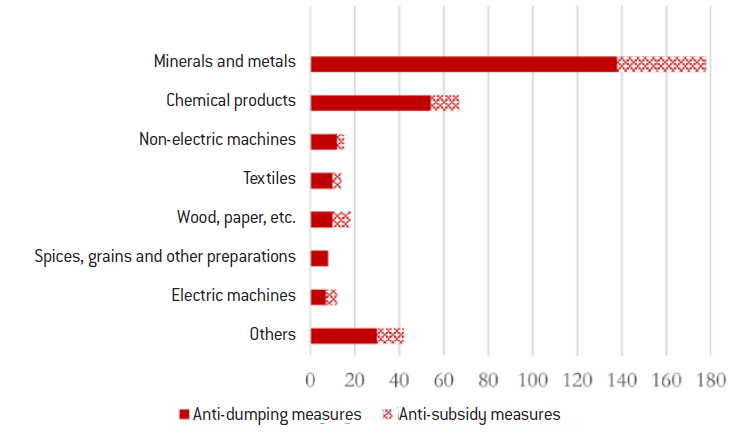

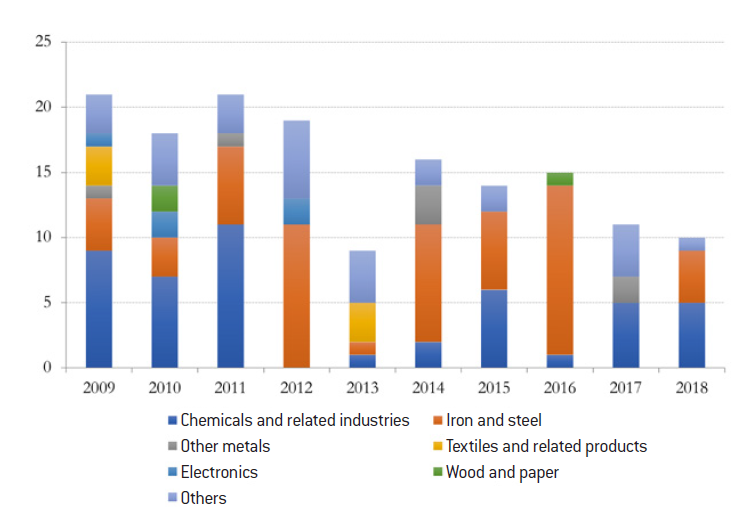

Sectoral targets for defence instruments, in number of measures in force at the end of 2018

Geographical and sectoral breakdown of new anti-dumping and anti-subsidy cases opened by the European Commission over the last ten years

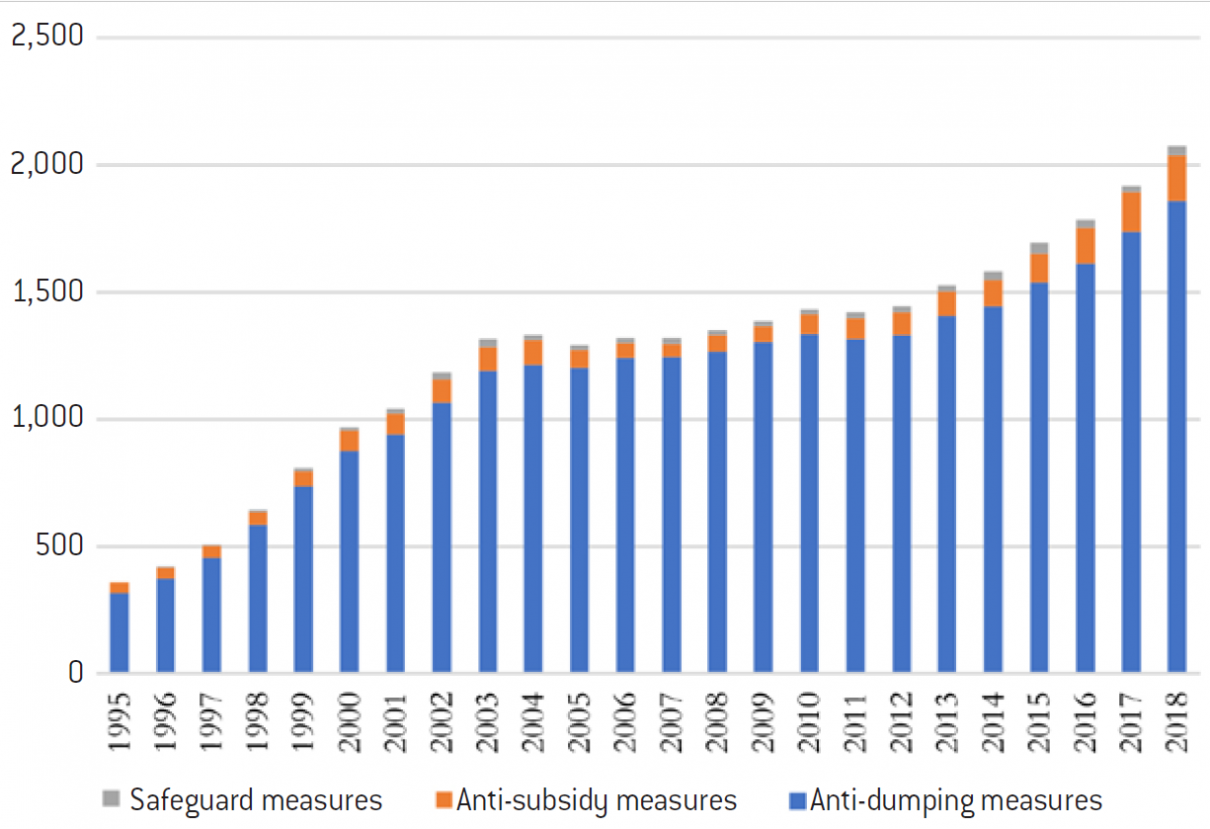

Trade defence instruments in force, all WTO members combined

Source :

WTO

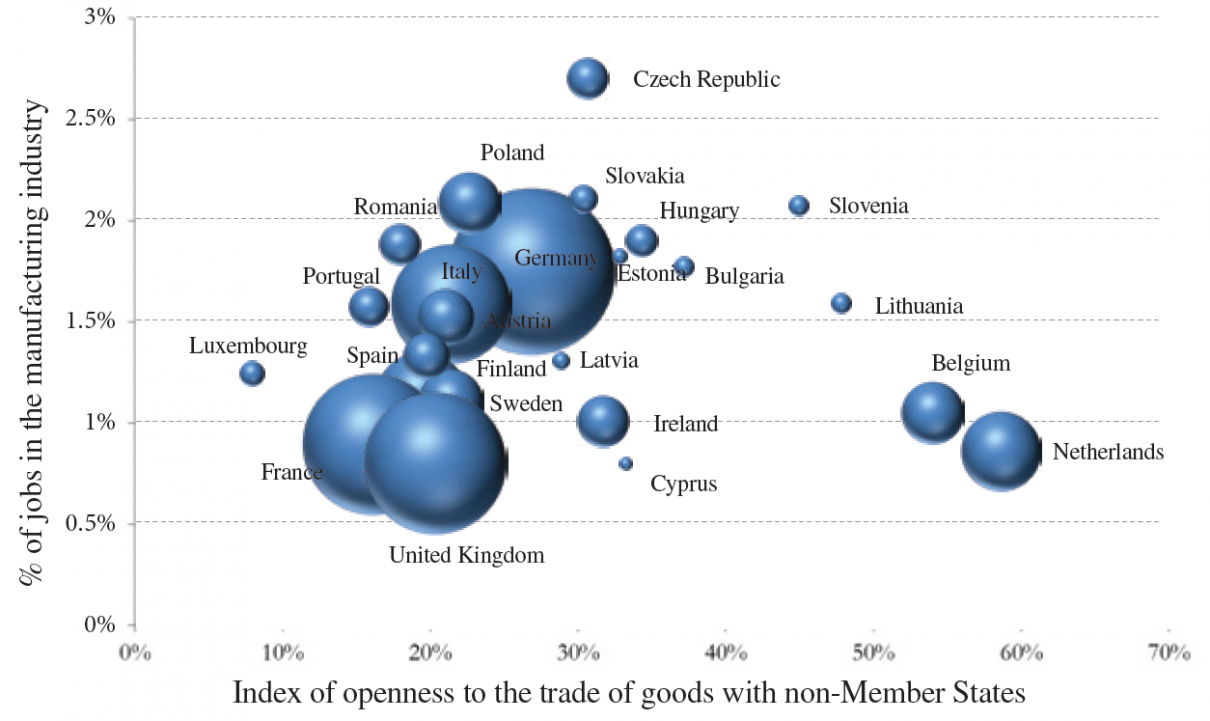

Positioning of Member States according to the size of their industry in terms of employment and their openness to trading goods with non-Member States (end of 2018)

Source :

Fondation pour l’innovation politique; data from the European Commission (Ameco database).

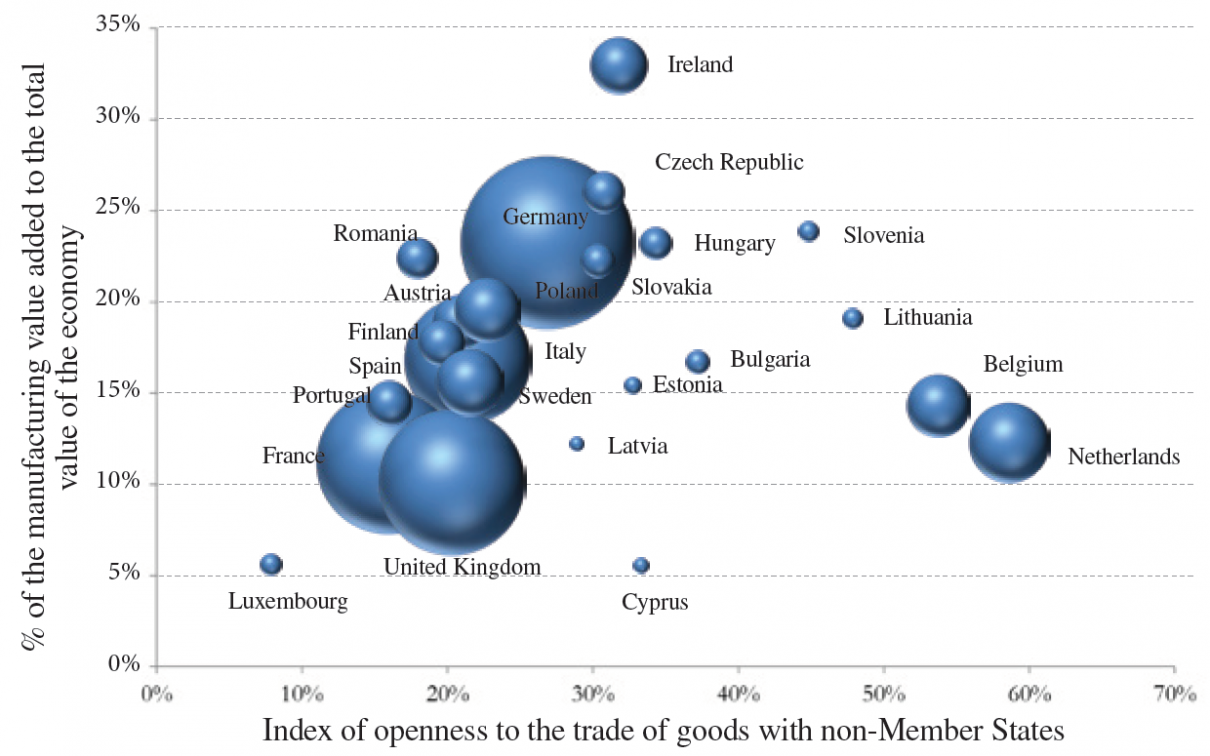

Positioning of Member States according to the size of their industry in terms of contribution to total value added and their openness to trading goods with non-Member States (end of 2018)

Source :

Fondation pour l’innovation politique; data from the European Commission (Ameco database).

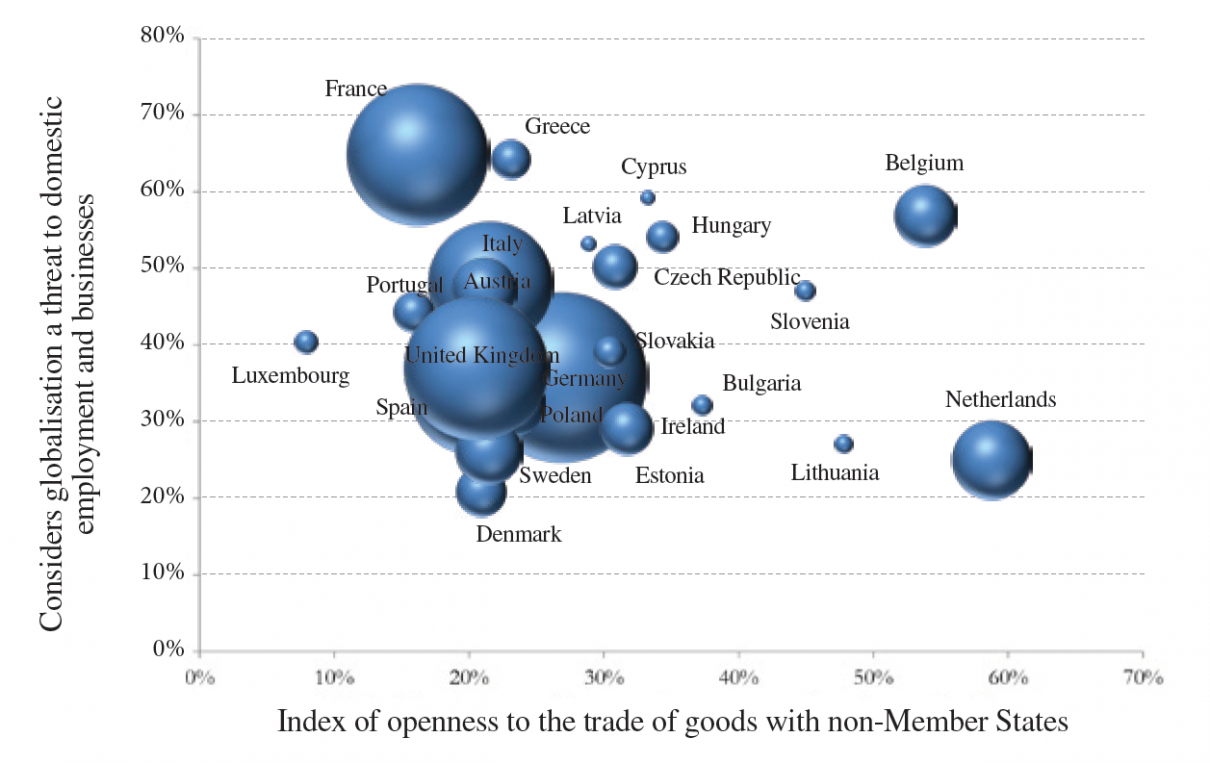

Member States’ positioning in terms of perceptions of globalisation and their openness to trading goods with non-Member States (end of 2018)

Source :

Fondation pour l’innovation politique; data from the European Commission (Ameco, Eurobarometer).

Note: The graphs were obtained on the basis of the populations of the Member States in 2018, by using the positions traditionally adopted by the Member States at the Council on trade defence issues. The positions used are those presented in the above-mentioned research projects. As data are only available for the fifteen members of the European Union of 1995 (EU15), we have assigned a “neutral” position by default to the other thirteen current members19.

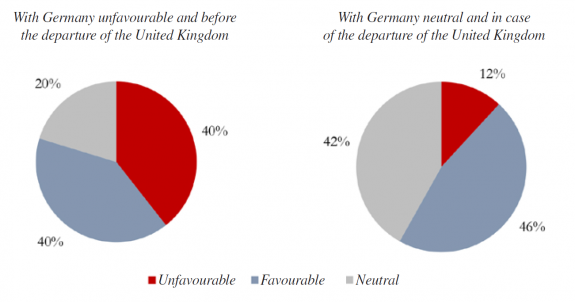

Distribution of traditional positions on trade defence at the Council in proportion to the population of each Member State

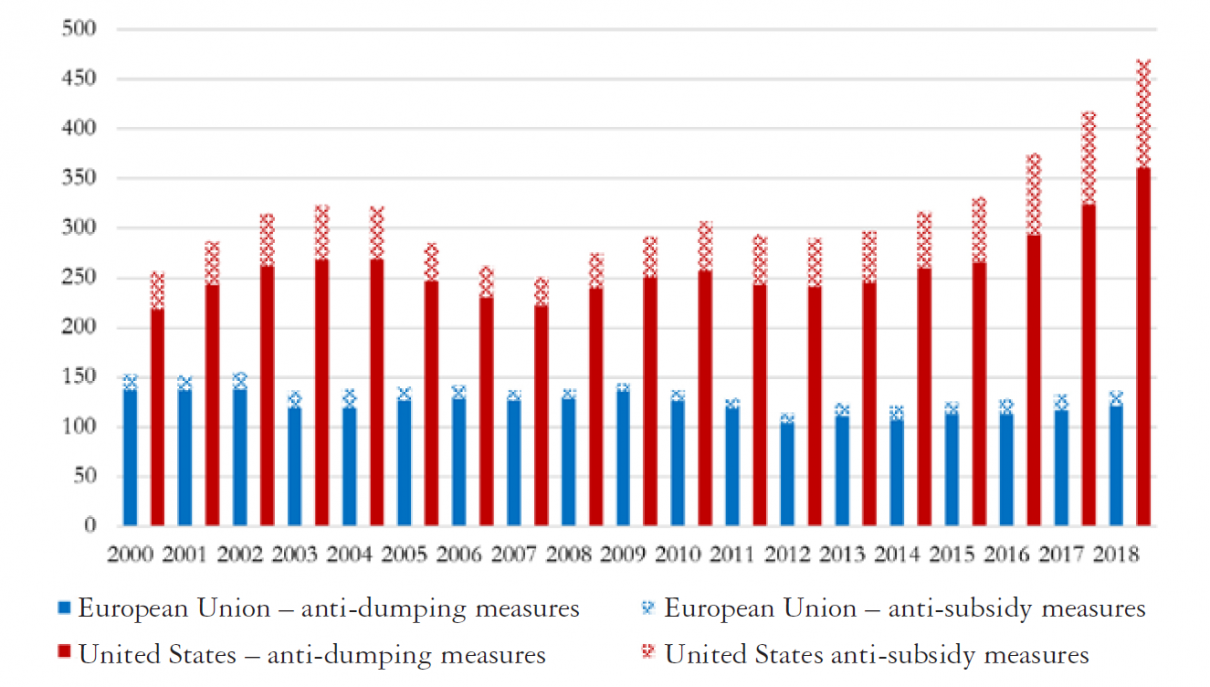

Trade defence instruments: number of measures in force in the United States vs. the European Union

Copyright :

Note: The WTO data used in this graph count the number of trade defence instruments in effect by taking into account the number of countries targeted by each instrument (an instrument on a given type of good targeting three separate countries simultaneously is therefore counted three times).

Source :

Fondation pour l’innovation politique; WTO data.

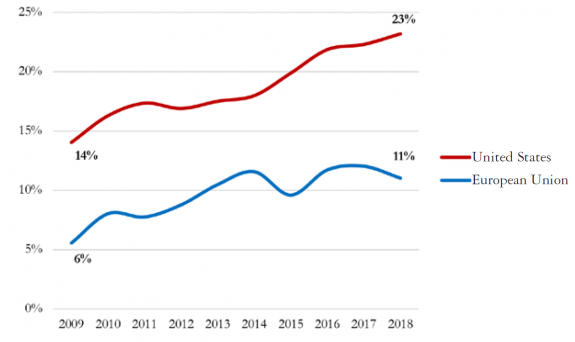

Undeniably, the United States seems increasingly ready to protect their domestic industries through corrective customs duties. To this end, we note an increasing use by the American administration – and more systematically than in Europe – of anti-subsidy instruments. In ten years, the proportion of anti-subsidy cases has increased from 14% to 23% in the United States. This development is also visible in Europe, although it seems to have slowed down over the last five years.

Share of anti-subsidy measures in the overall measures in effect (with the exception of safeguard measures)

Source: Fondation pour l’innovation politique; WTO data.

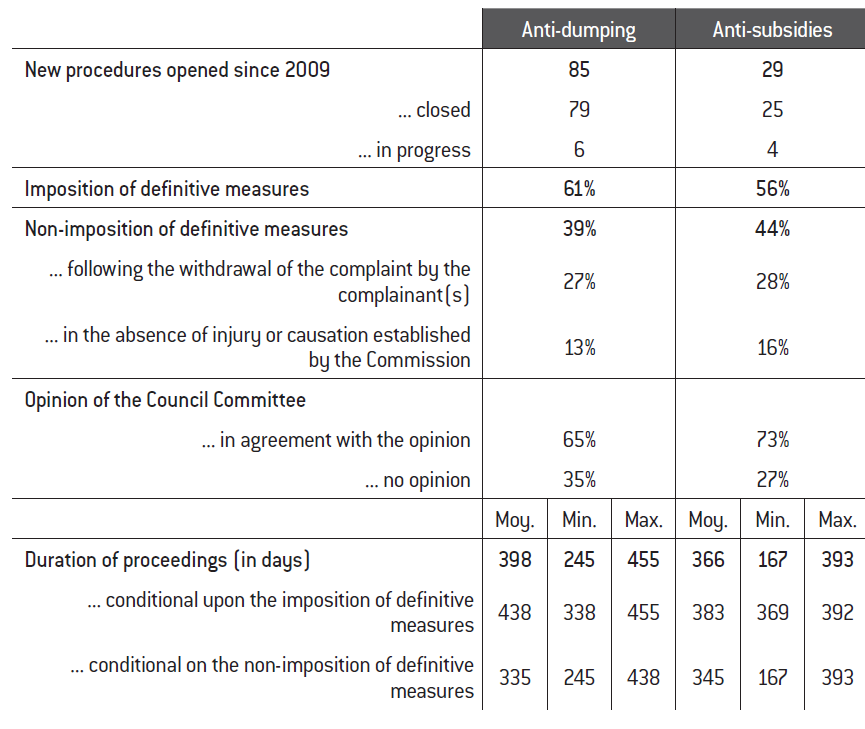

Review of the anti-dumping and anti-subsidy proceedings initiated by the European Commission from January 2009 to the end of November 2019

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union

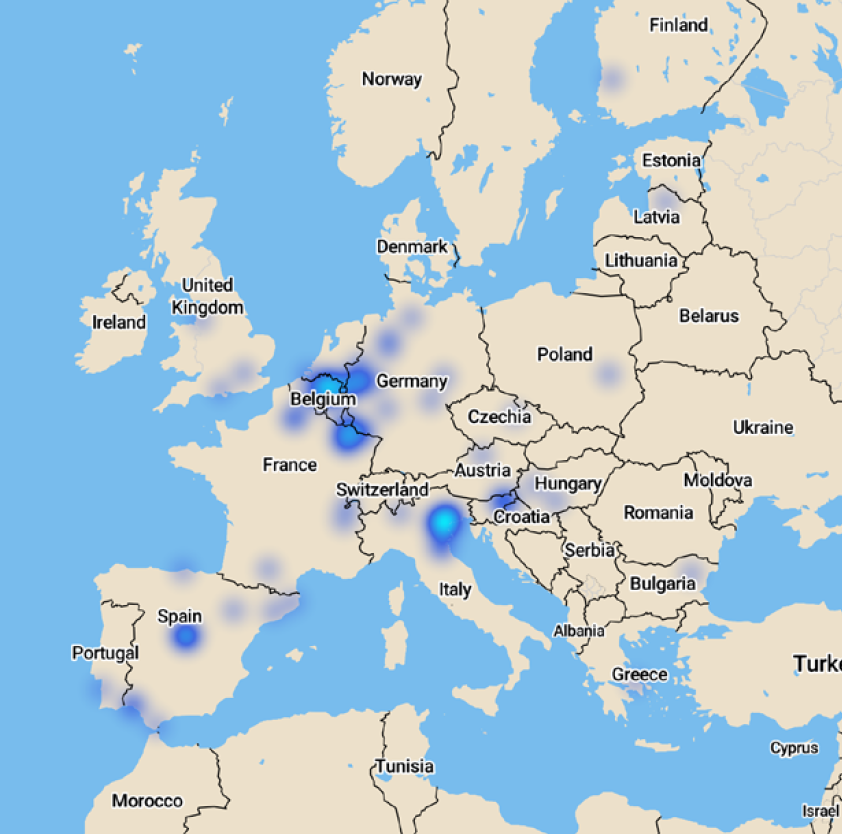

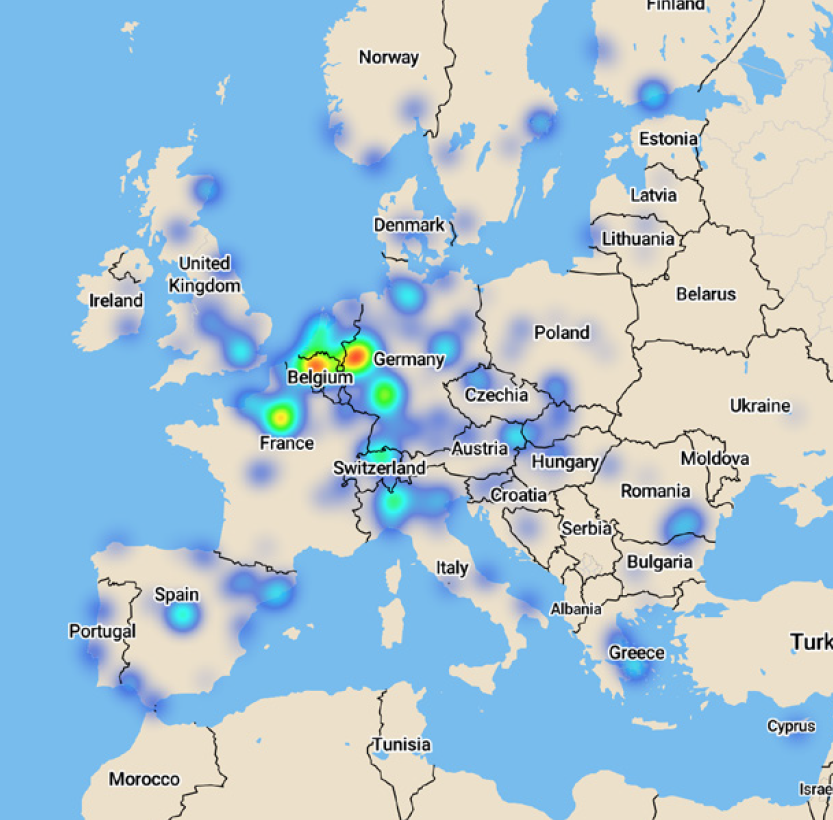

Location of the head offices of the complaining companies named in the anti-dumping and anti-subsidy investigations

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union, Google Maps, Mapbox, OpenStreetMap.

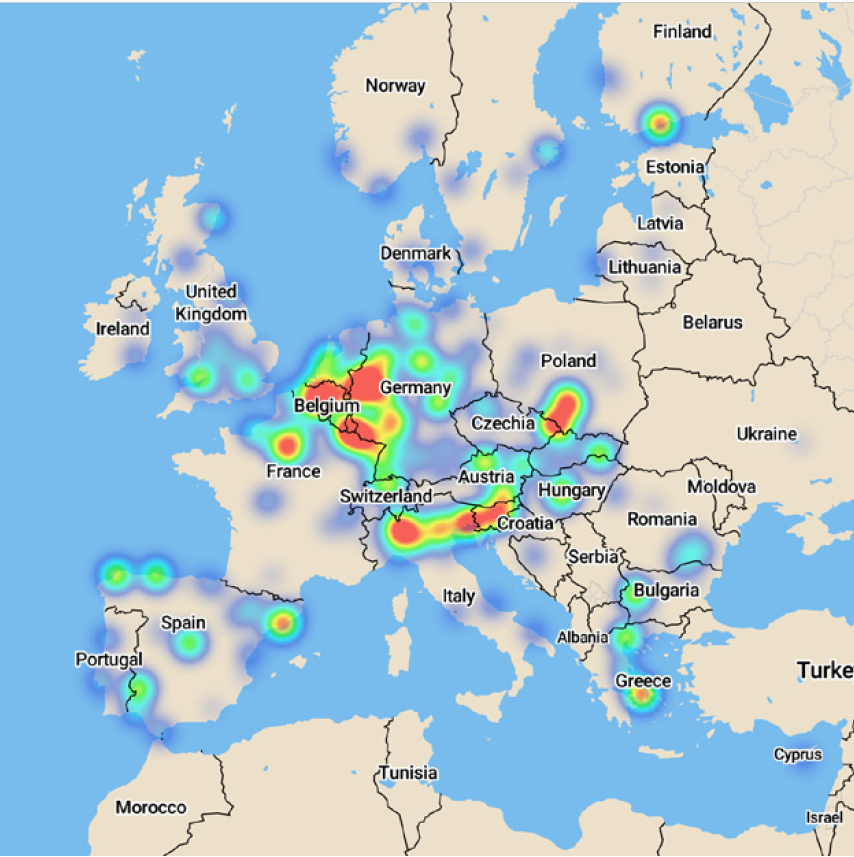

Location of the head offices of the complaining companies named or members of a European association representing their interests

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union, Google Maps, Mapbox, OpenStreetMap.

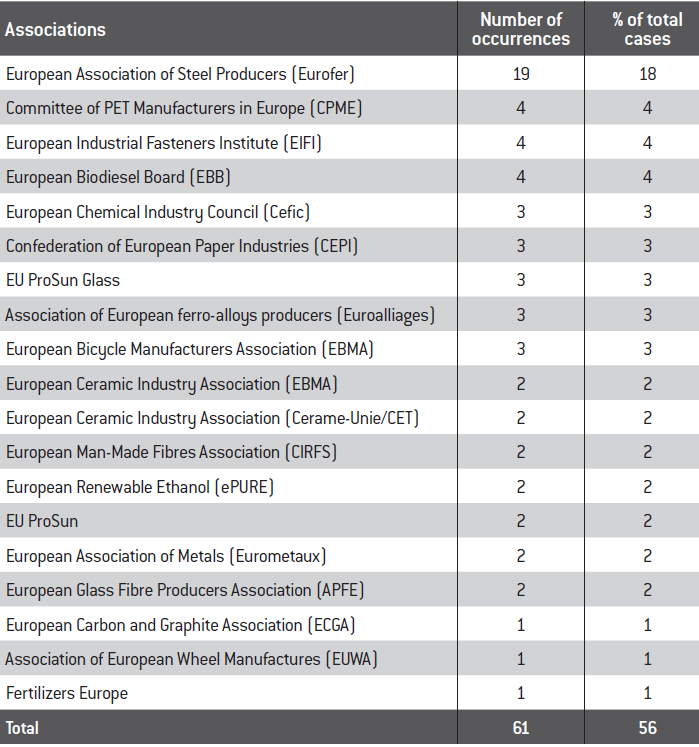

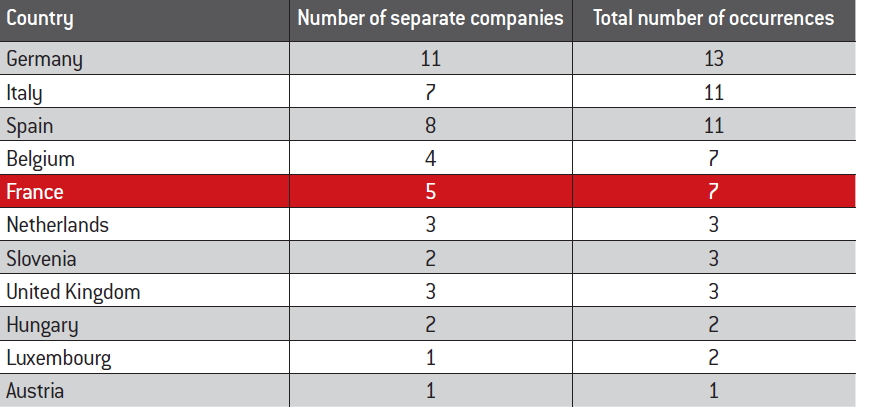

European producers’ associations responsible for cases opened by the European Commission over 2009-2019

Source :

Fondation pour l’innovation politique; data Official Journal of the European Union.

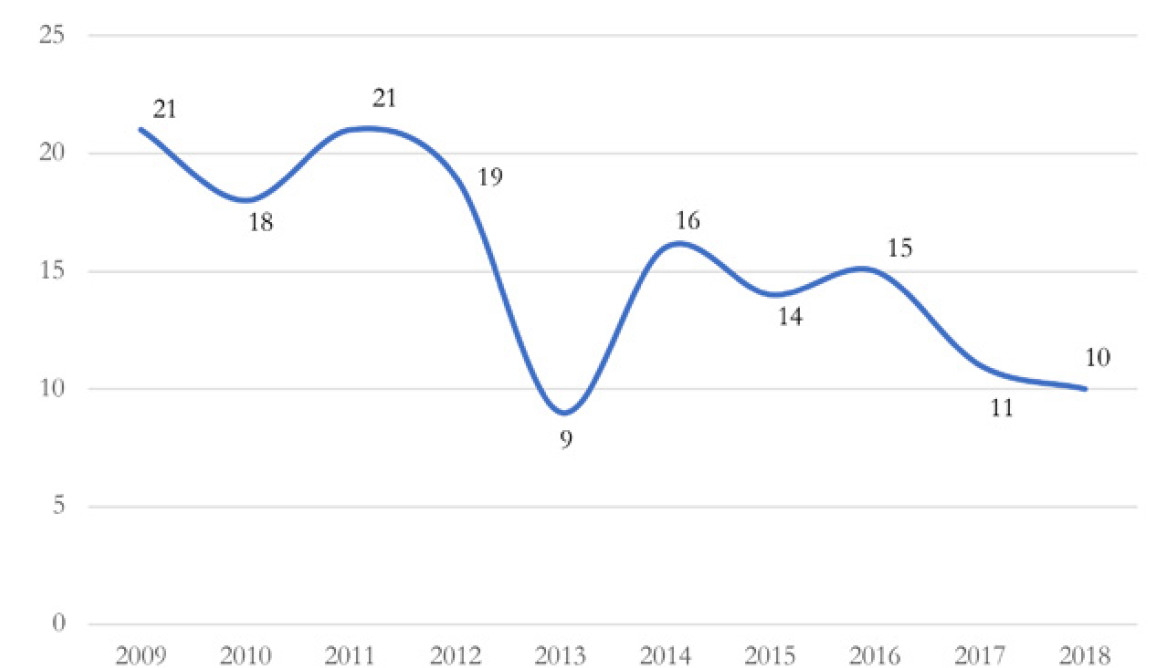

New anti-dumping and anti-subsidy investigations initiated by the European Commission (excluding the re-openings of past investigations)

Source :

Official Journal of the European Union.

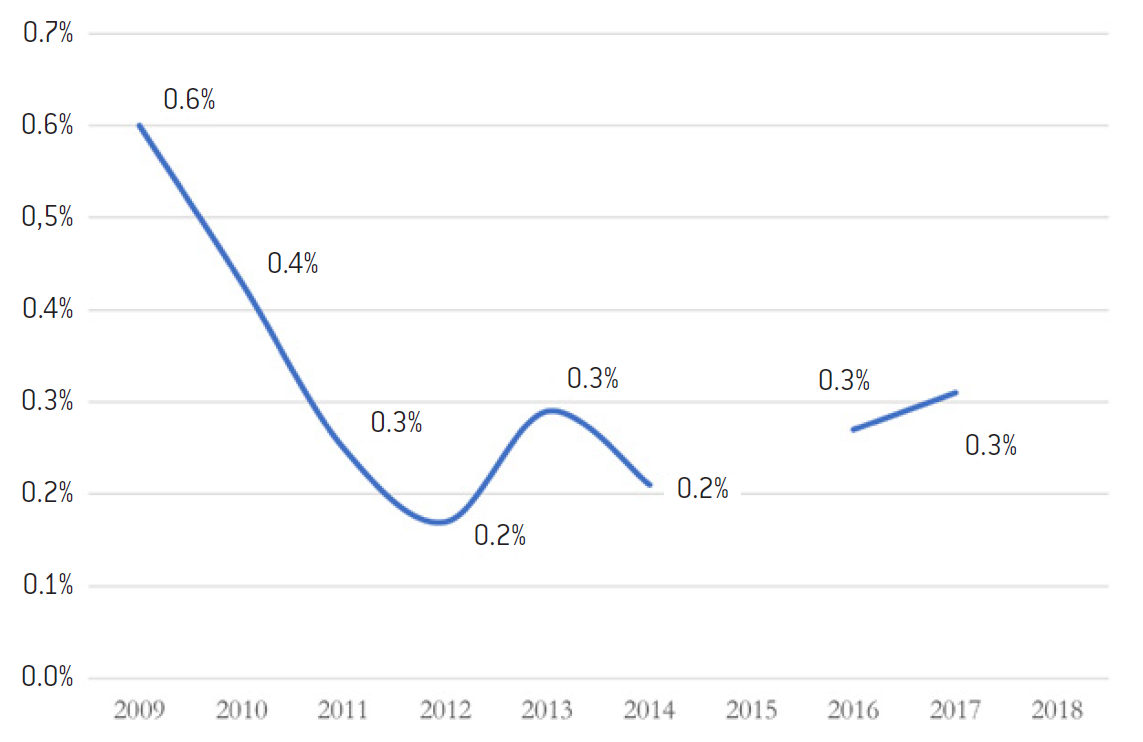

Share of total imports into the European Union affected by anti-dumping and anti-subsidy duties

Source :

Source: Annual reports from the European Commission to the Council and the European Parliament on the European Union’s anti-dumping, anti-subsidy and safeguard activities.

Note: Data for the years 2015 and 2018 are missing as they are not disclosed in the annual reports.

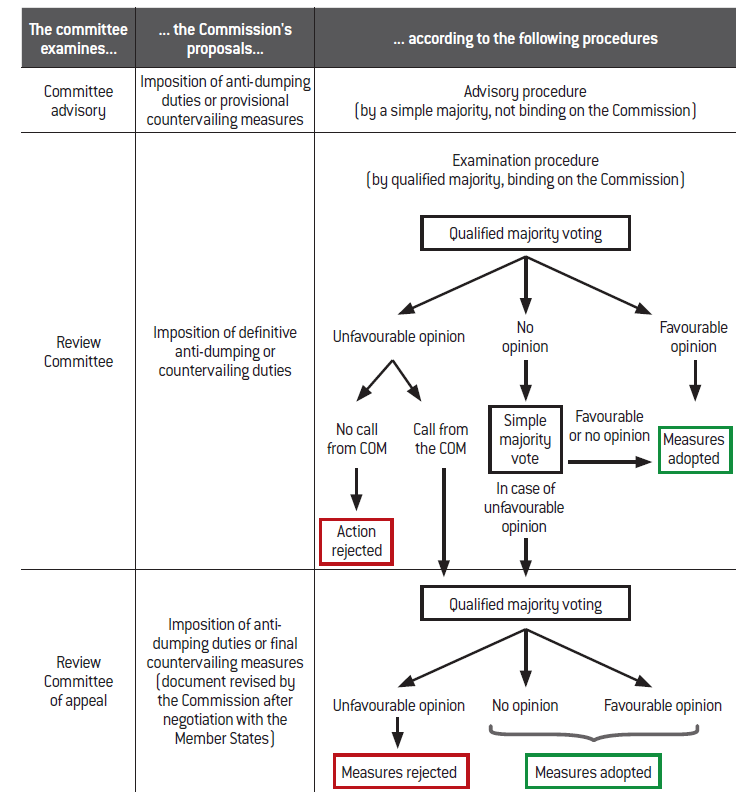

Outline of the European decision-making procedure in anti-dumping and anti-subsidy cases

Source :

Fondation pour l’innovation politique.

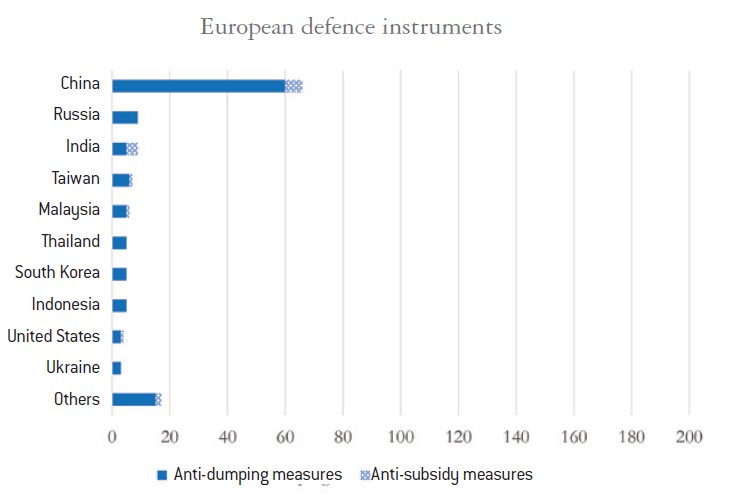

European defense instruments

Source :

Fondation pour l’innovation politique; WTO data.

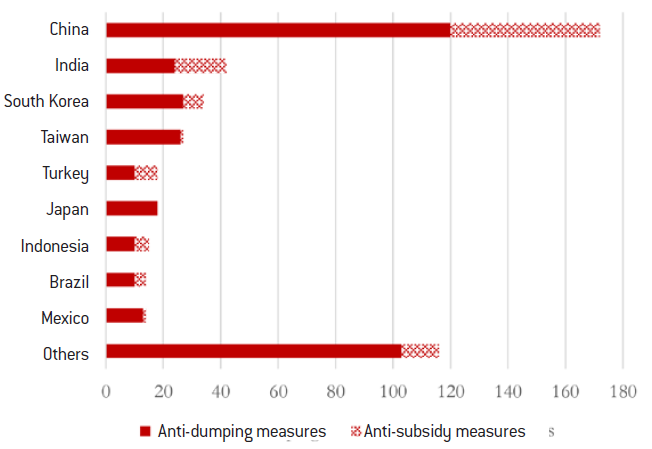

U.S. defence instruments

Source :

Fondation pour l’innovation politique; WTO data.

European defense instruments

Source :

Fondation pour l’innovation politique; WTO data.

U.S. defence instruments

Source :

Fondation pour l’innovation politique; WTO data.

The top five exporting countries targeted by the investigations opened by the European Commission over the last ten years are, in descending order, China (41% of new investigations), India (11%), Russia (5%), Turkey (4.5%) and Indonesia (4%).

Source :

Fondation pour l’innovation politique; WTO data.

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union.

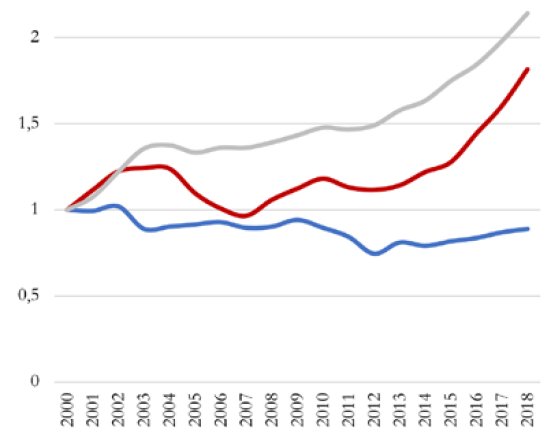

Trade defence instruments: number of measures in force per importing country (base 1 in 2000)

Source :

Fondation pour l’innovation politique; WTO data.

Location of the registered offices of the complaining companies named or members of a European association representing their interests, excluding Eurofer

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union, Google Maps, Mapbox, OpenStreetMap.

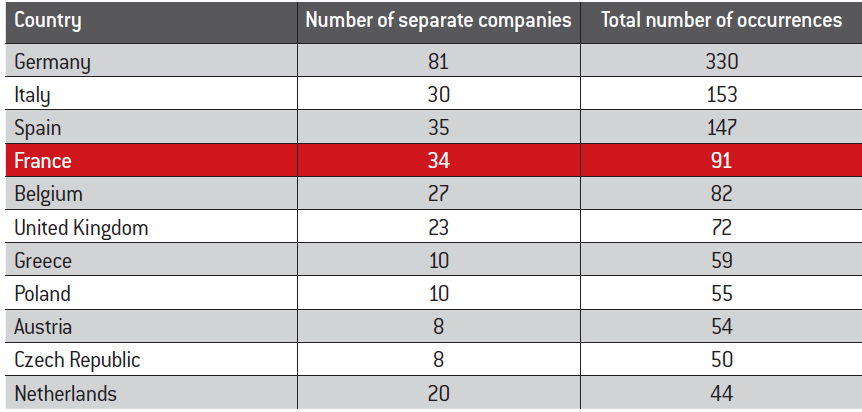

Location of the head offices of the complaining companies named in the anti-dumping and anti-subsidy investigations initiated by the European Commission over the last ten years

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union.

Location of the head offices of the complaining companies or members of European associations named in the anti-dumping and anti-subsidy investigations initiated by the European Commission over the last ten years.

Source :

Fondation pour l’innovation politique; data from the Official Journal of the European Union.

No comments.