The imperative end of "helicopter money"

Jean-Baptiste Wautier, a Private Equity investor, is the author of the analysis "The imperative end of helicopter money" published by the Fondation pour l’innovation politique.

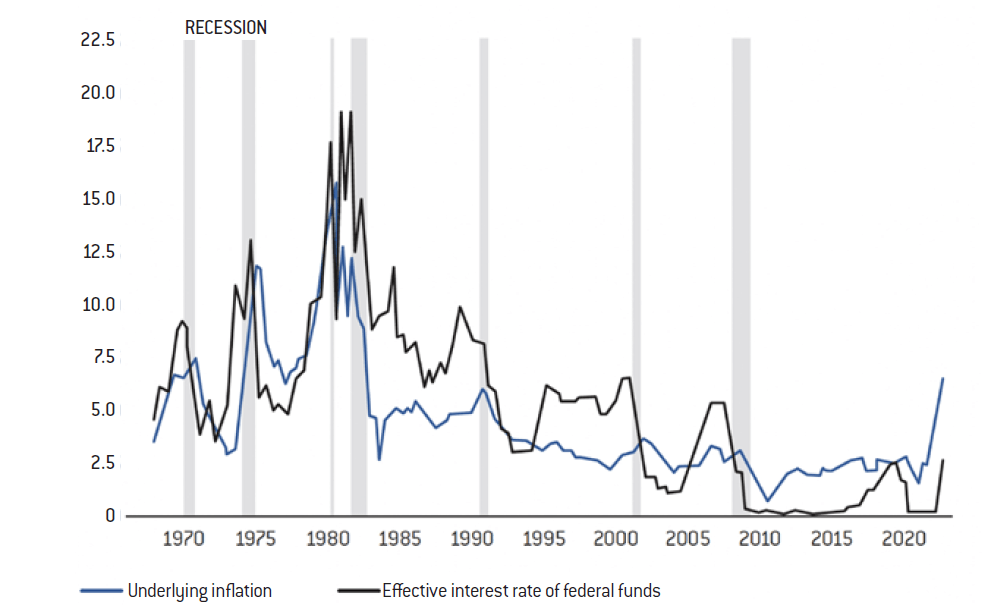

Effective federal funds interest rates (in %)

Source :

FRED

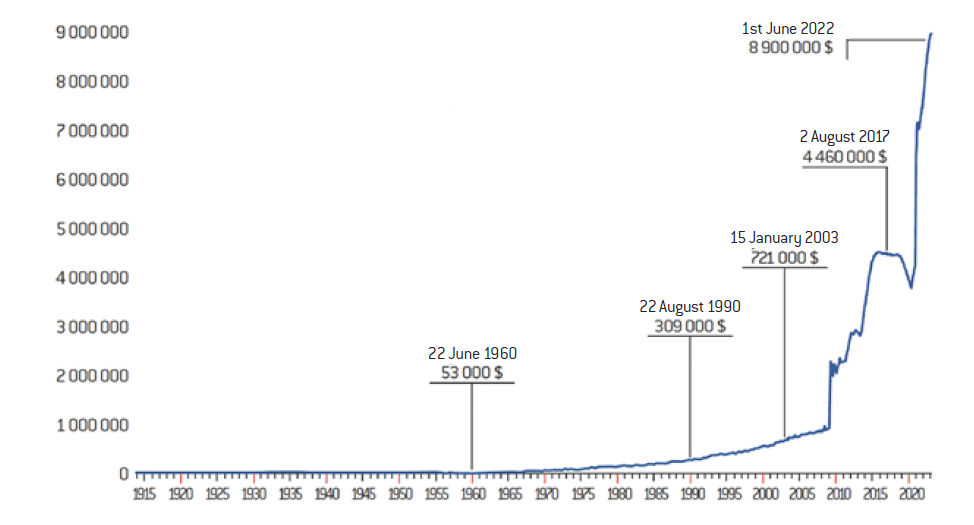

Federal Reserve Balance Sheet, 1914-2020 (in millions of dollars)

Source :

Center for Financial Stability

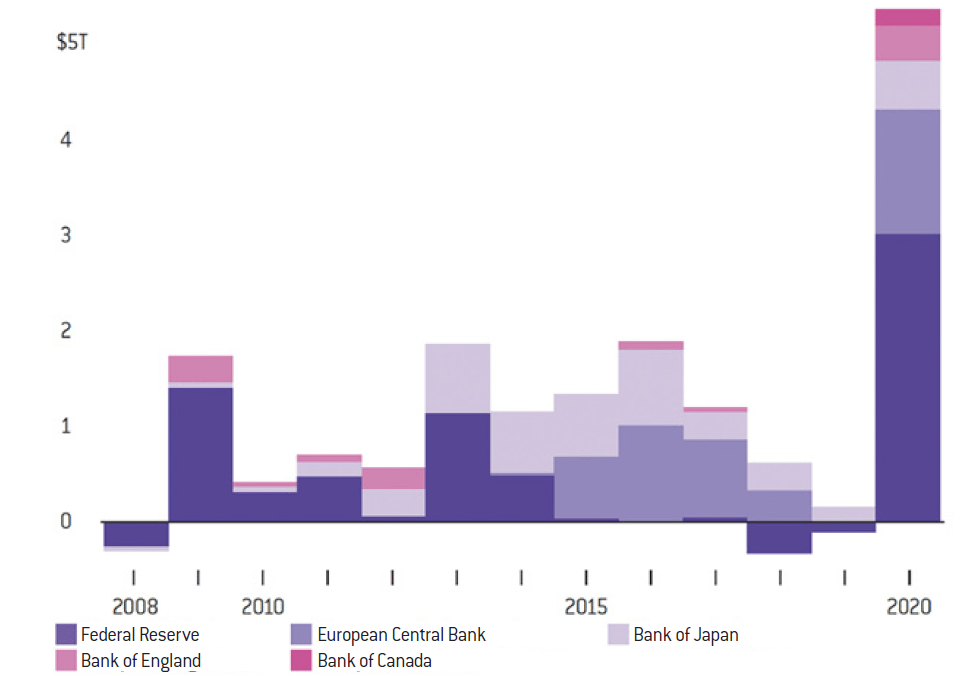

The surge in purchases – Central banks have stepped up their asset purchases to support governments’ response to the pandemic

Source :

Data compiled by Bloomberg

Note: Figures represent values converted to USD from local currencies

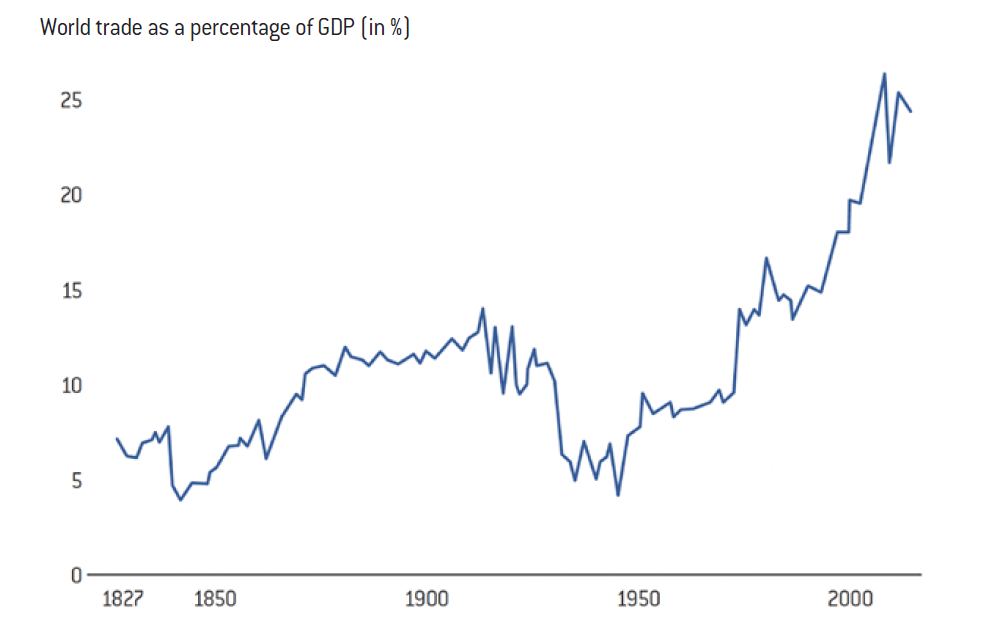

Globalisation is at an all-time high, and has not shown any sign of reversion

Source :

Michel Fouquin and Jules Hugot, Centre d’études prospectives et d’informations internationales, 2016 ; data from « Our world in data »

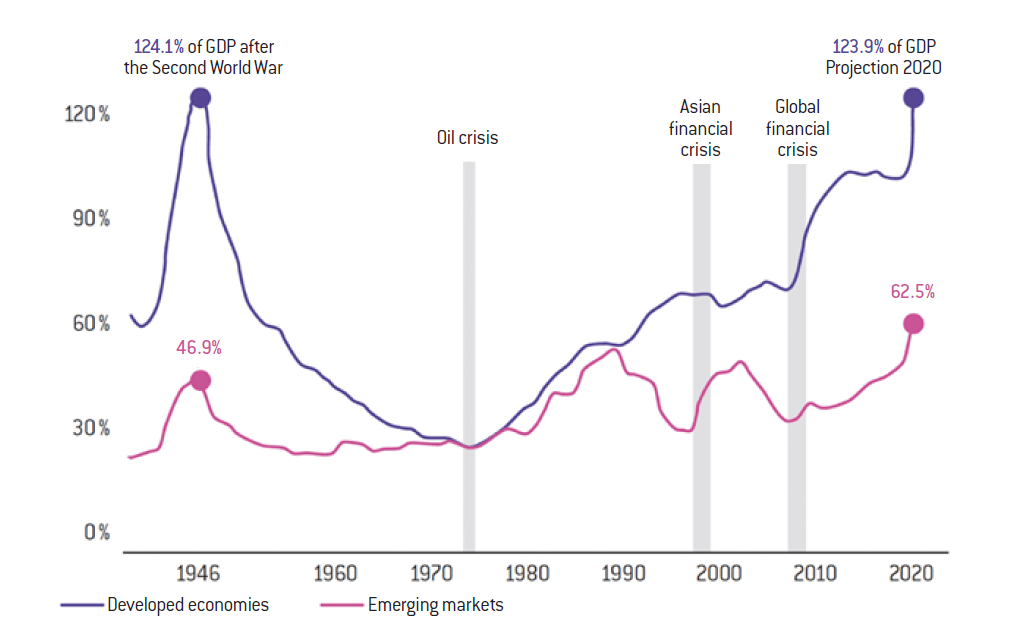

The Great Debt Spike – GFC and Pandemic led to historic levels of Debt/GDP

Source :

International Monetary Fund Fiscal Monitor, October 2020

Note: Advanced economies and emerging markets are a sample of 25 and 27 countries respectively.

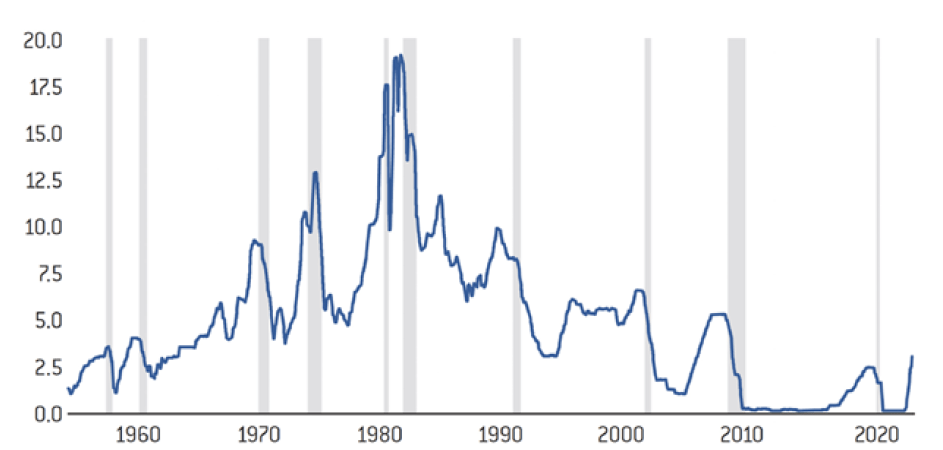

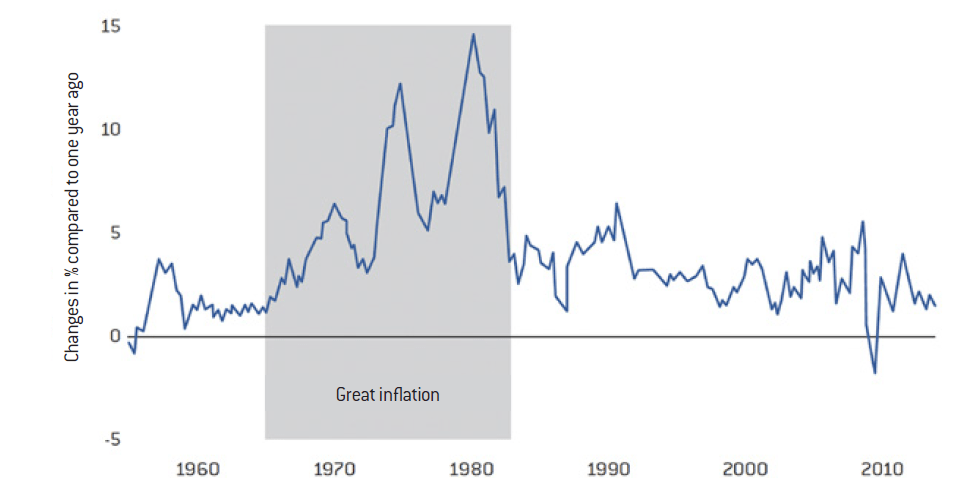

Inflation measured by the consumer price index

Source :

FRED

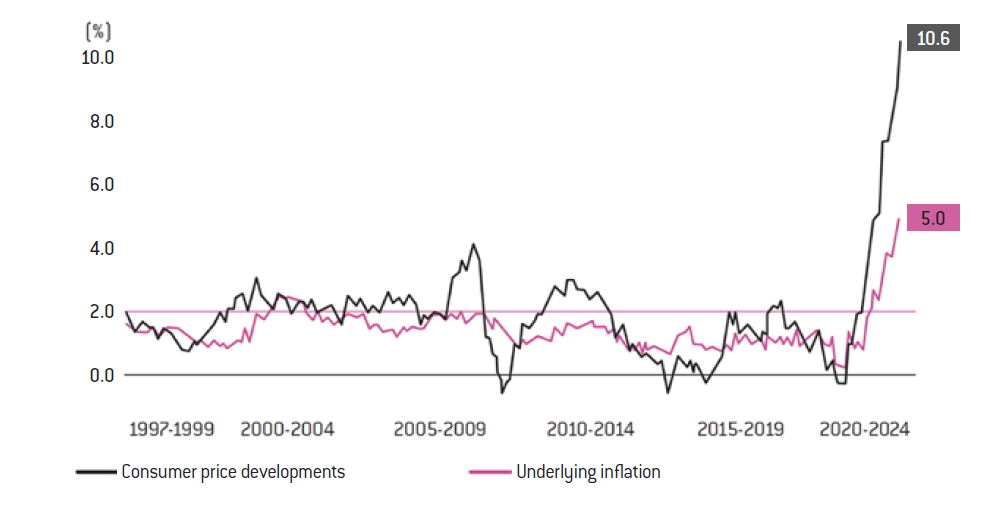

Inflation reached 10.6% in the eurozone

Source :

Eurostat

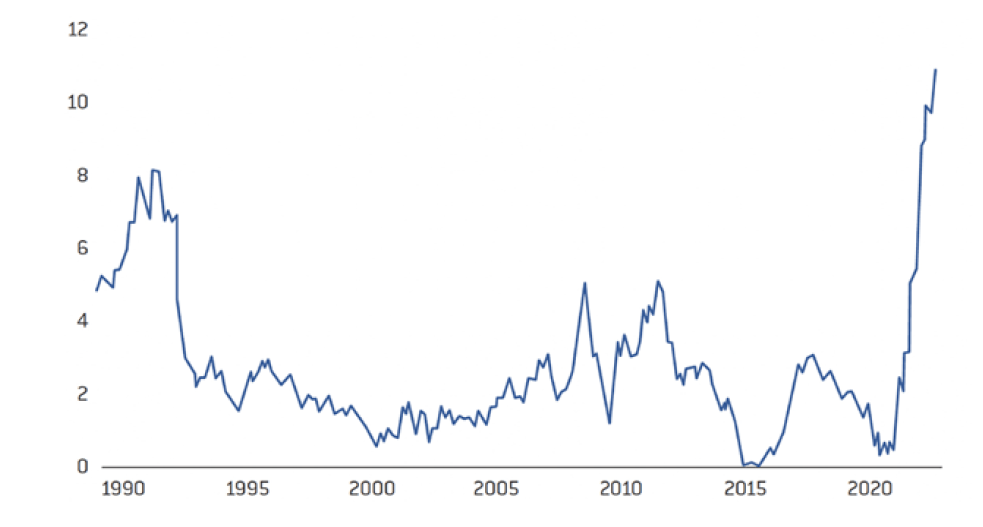

United Kingdom: Consumer price index, 12-month change (%)

Source :

Office for National Statistics

Blame the lag: every Fed chairman since the 1970s has raised rates right up to the time of the recession, then lowered them considerably – The Fed’s response to inflation (in %)

Source :

Federal Reserve Board, Federal Reserve Bank of Atlanta

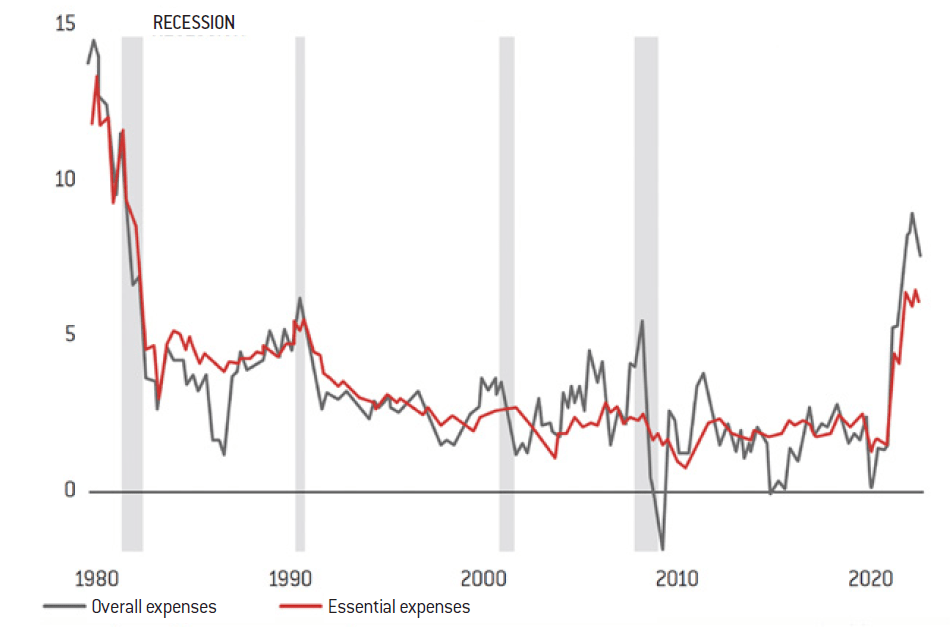

US consumption index, change from previous year (%)

Source :

Labor Department

Note: The “essential expenditure” curve excludes food and energy prices.

German producer prices are rising at a record pace – Annual % change in industrial product prices

Source :

Destatis, Refinitiv

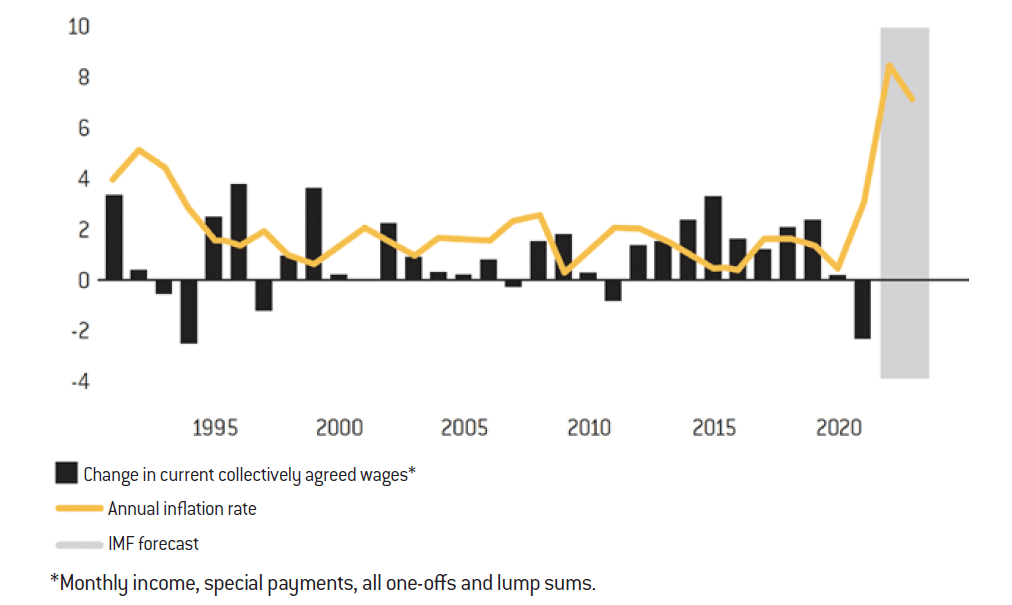

Wage agreements for the German metal and electrical industries (in %)

Source :

IG Metall, World Bank, IMF

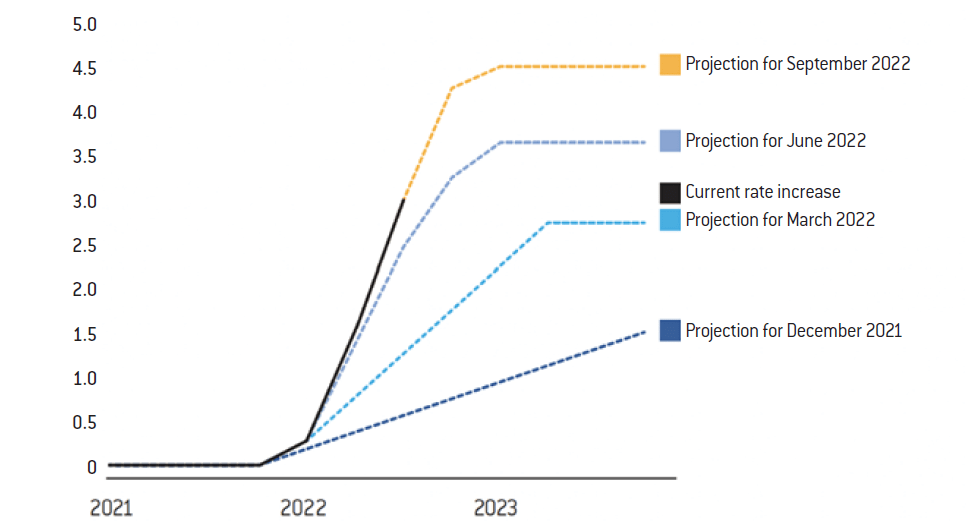

Fed rate hike expectations (in %) – Fed officials have raised their estimates of their rate hike policy

Source :

Federal Reserve

Note: Policy rate projections reflect the Fed’s positioning on averages.

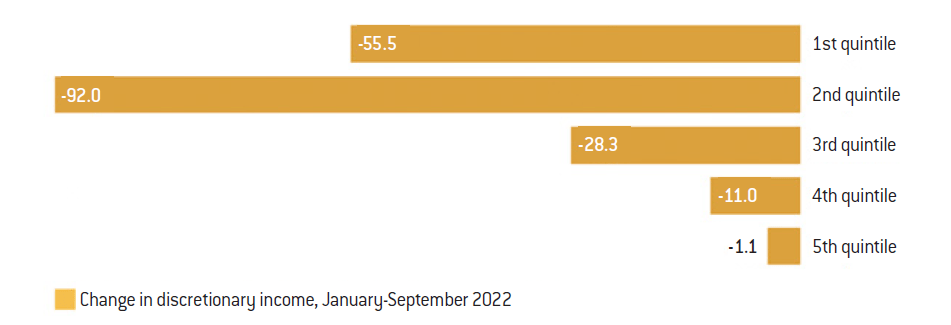

Nothing left – Discretionary income of the second quintile of earners has fallen since the beginning of the year in the UK

Source :

Asda Income Tracker, Center for Economics and Business Research

Note: Discretionary income is the amount of money available in a household after subtracting taxes and essential expenses.

Lowest incomes – Inflation has disproportionately hit the purchasing power of the poorest families in the UK (in %)

Source :

Asda Income Tracker, Cebr

Outstanding credit cards are on the rise (in billions of dollars)

Source :

Federal Bank of New York

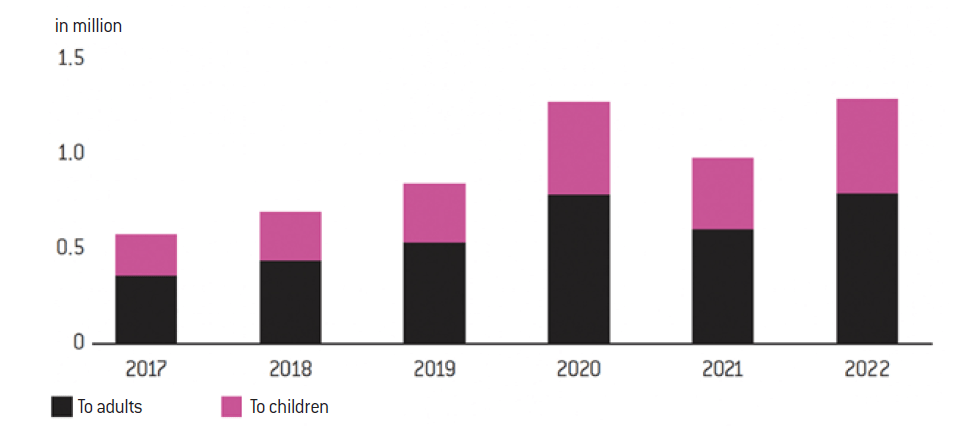

A tsunami of need – Almost 1.3 million emergency food parcels have been distributed

in the UK

Source :

Trussel Trust

Note: The figures show, for each year, the number of parcels distributed across the UK between April and September.

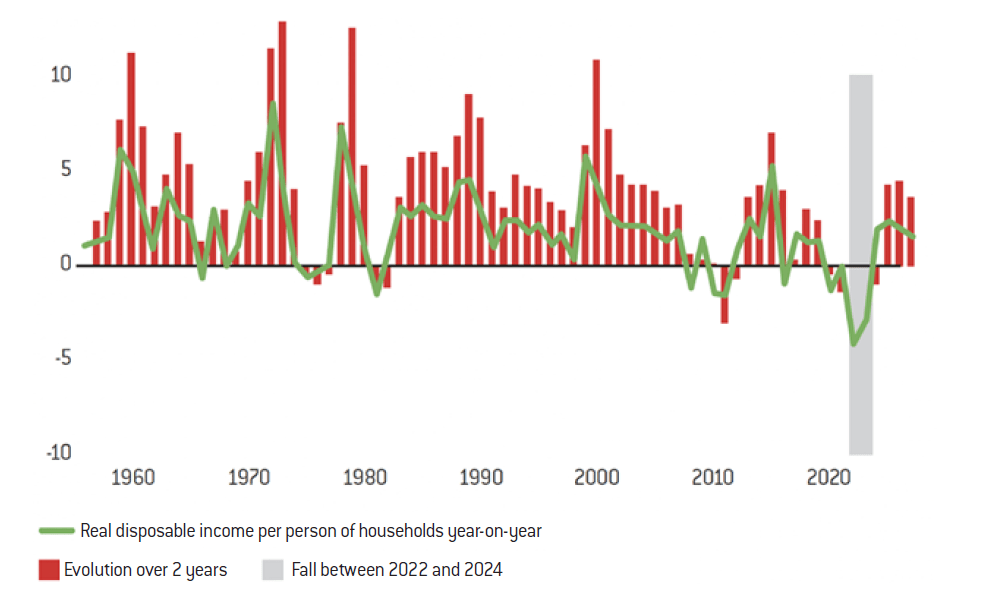

Sharp contraction – The UK is experiencing the biggest fall in living standards on record

Source :

Office for Budget Responsibility

Note: Forecasts from 2022-2023

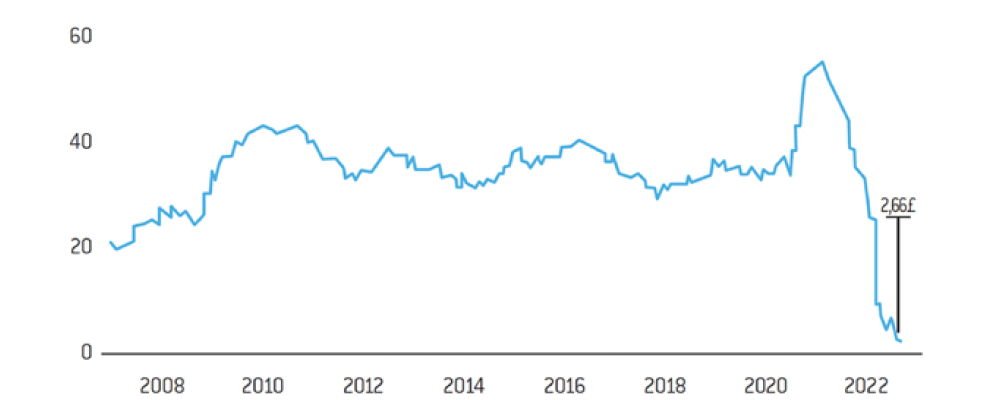

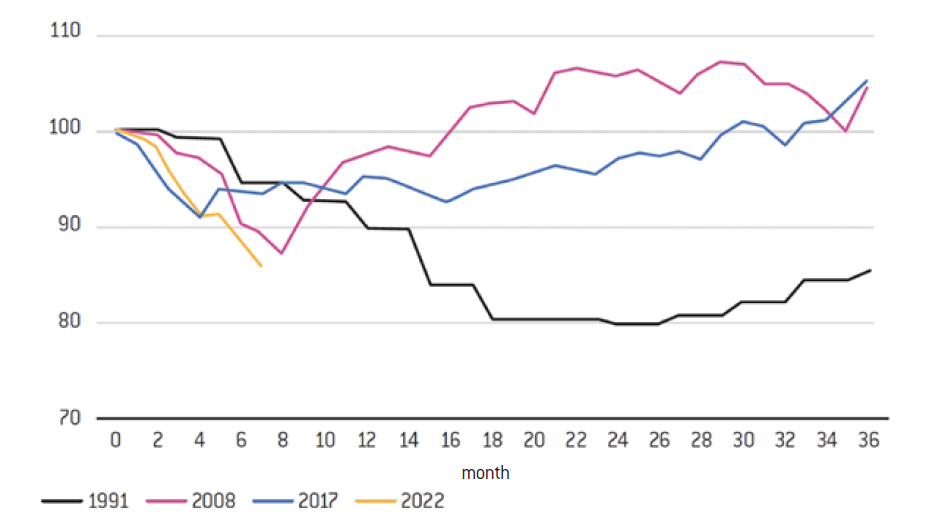

A rapid fall – Swedish house prices are in the worst slump since the early 1990s

Source :

Statistics Sweden, Valueguard

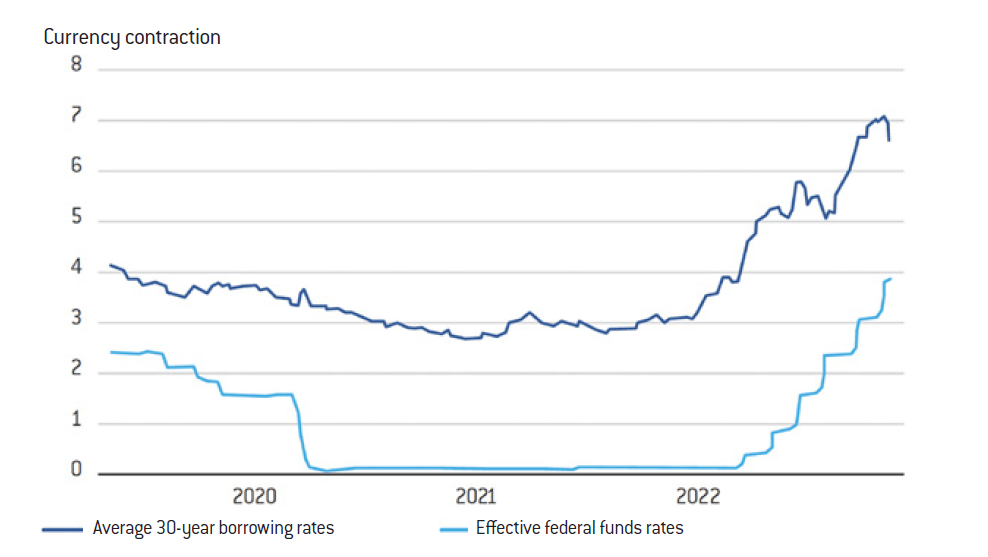

Evolution of US household borrowing rates

Source :

Freddie Mac, Federal Reserve

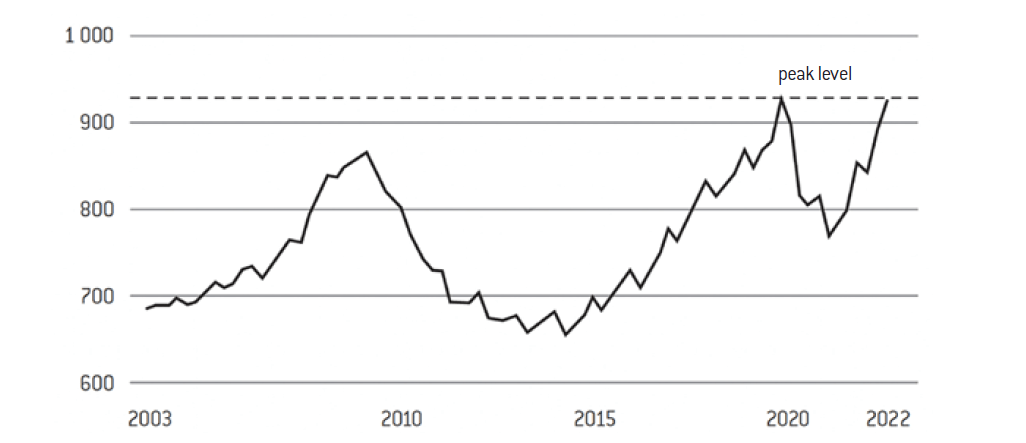

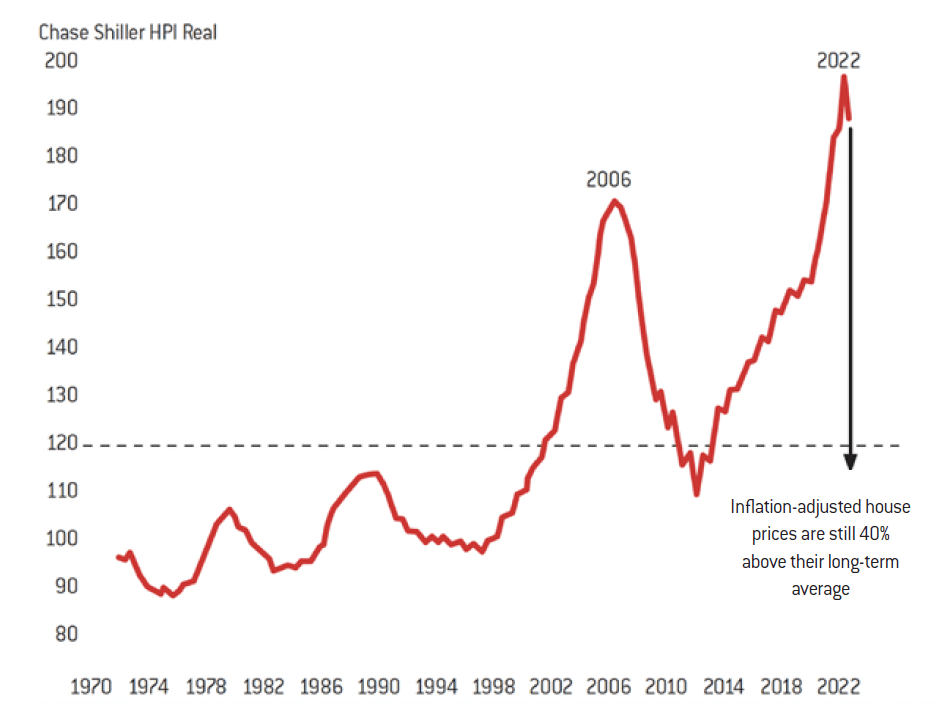

The housing bubble is bigger than ever – Inflation-adjusted house prices

Source :

Reventure Consulting (indice Case Shiller)