Europe in the face of American and Chinese economic nationalisms (1)

Competition policy and European industry

General introduction

Creating industrial champions to boost exports? Beware of the “PSG syndrome”

European intransigence in merger control: an idea to be put into perspective

Necessary incremental adaptations to merger control in a rapidly changing environment

European state aid control, a thorn to be removed as soon as possible?

Appendices

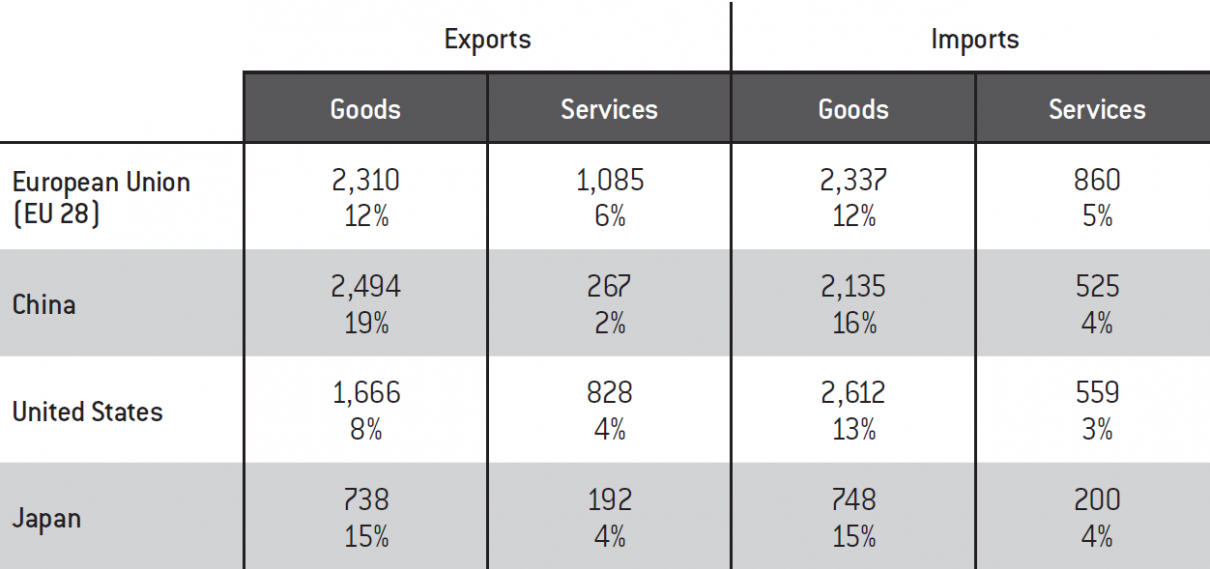

Main European Trading Partners

Global Performance of European Industry

Europe in the face of American and Chinese economic nationalisms (2)

Europe in the face of American and Chinese economic nationalisms (3)

Big tech dominance (1): the new financial tycoons

Big tech dominance (2) : a barrier to technological innovation ?

Towards personalised pricing in the digital era ?

International trade in 2018 (flows in billions of dollars and as a percentage of GDP)

Source :

Fondation pour l’innovation politique; data International Trade Centre, Eurostat.

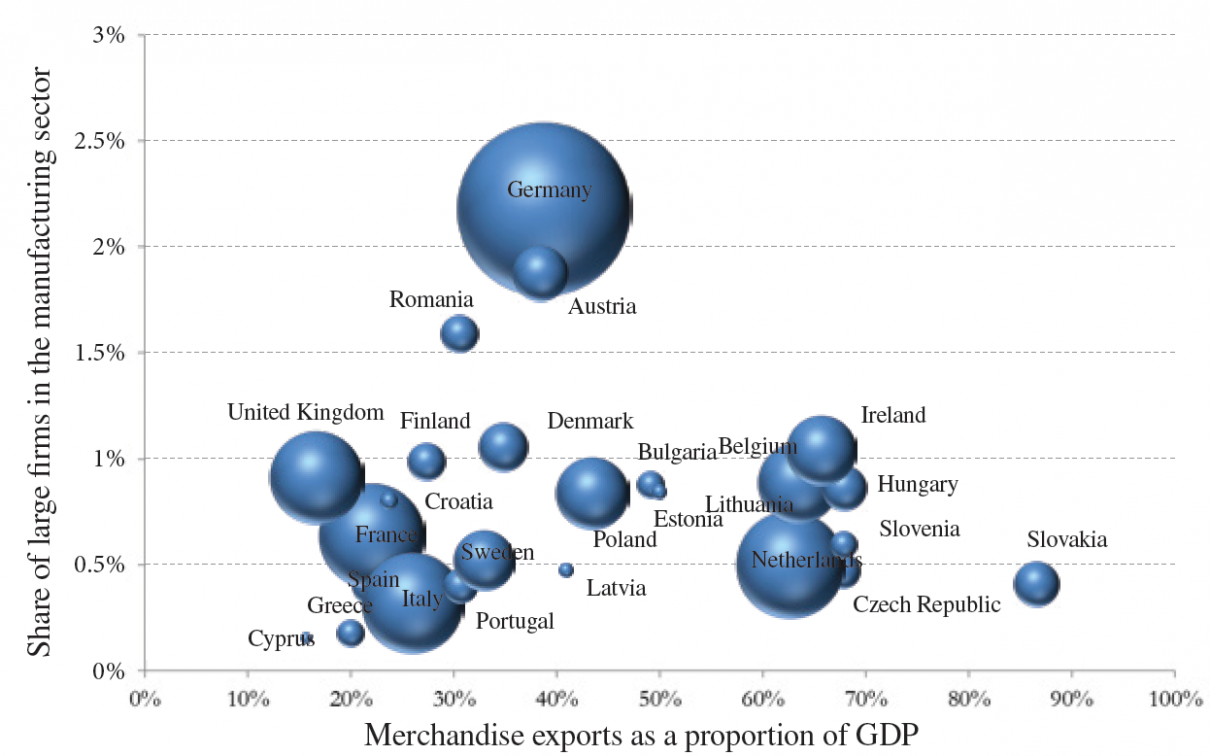

The relationship between the size of manufacturing firms and export performance

Copyright :

Note: The share of large firms in the manufacturing sector corresponds to the percentage of firms with more than 250 employees in the sector.

Source :

Fondation pour l’innovation politique; Eurostat data.

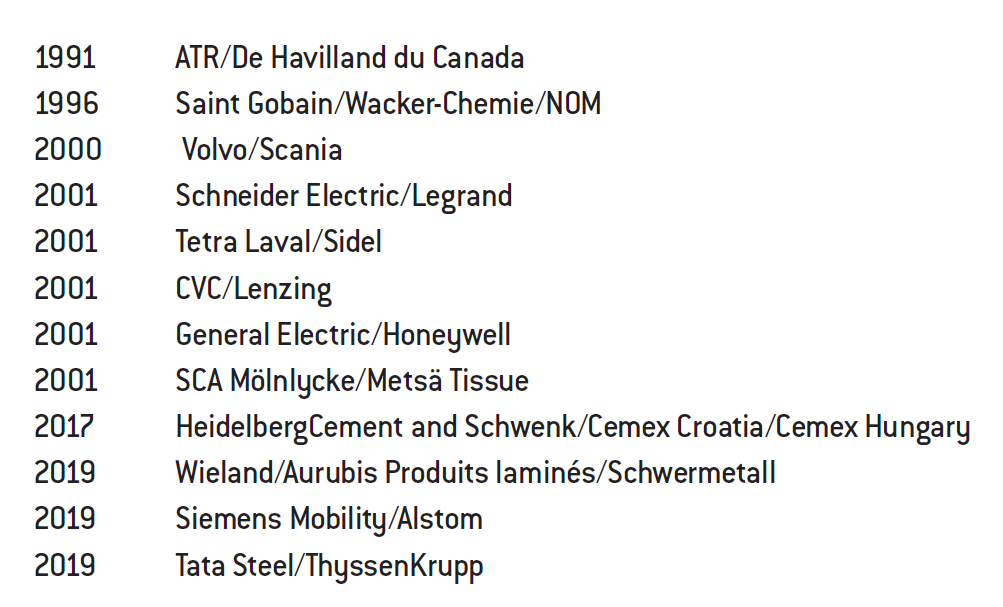

Industrial concentrations prohibited by the European Commission since 1989

Source :

European Commission.

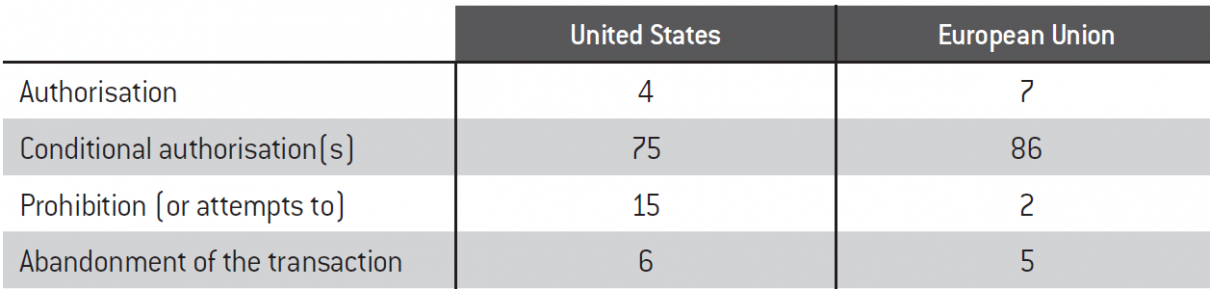

Results of in-depth merger control investigations (average 2014-2018), all sectors combined(%)

Source :

Fondation pour l’innovation politique; Dechert LLP (DAMITT) data.

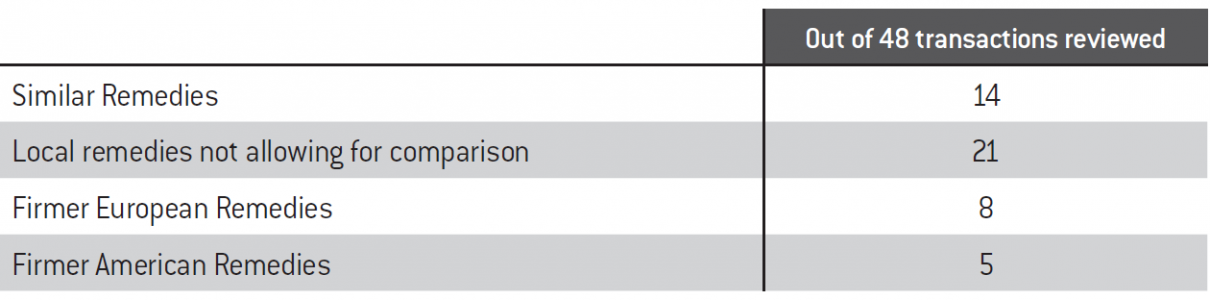

Comparison of remedies imposed during industrial concentrations (on a sample of industrial transactions with a global impact, from 2000 to 2018)

Source :

Fondation pour l’innovation politique.

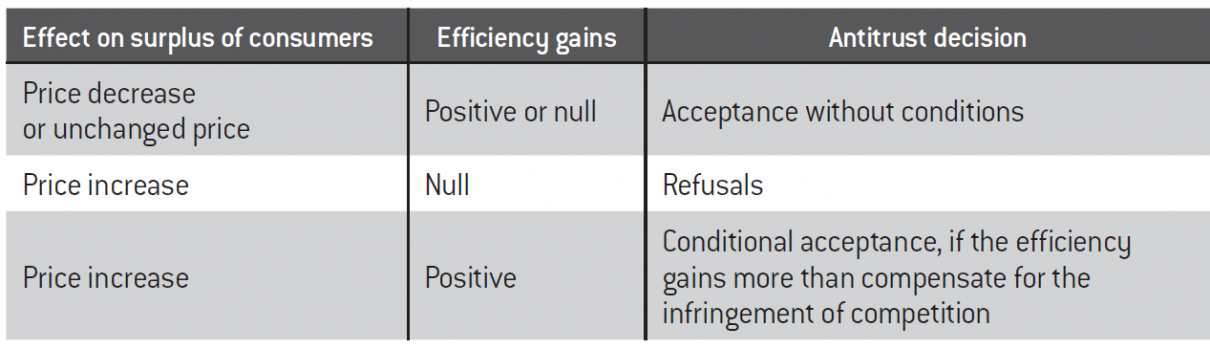

Implications of Oliver Williamson’s analysis

Source :

Fondation pour l’innovation politique.

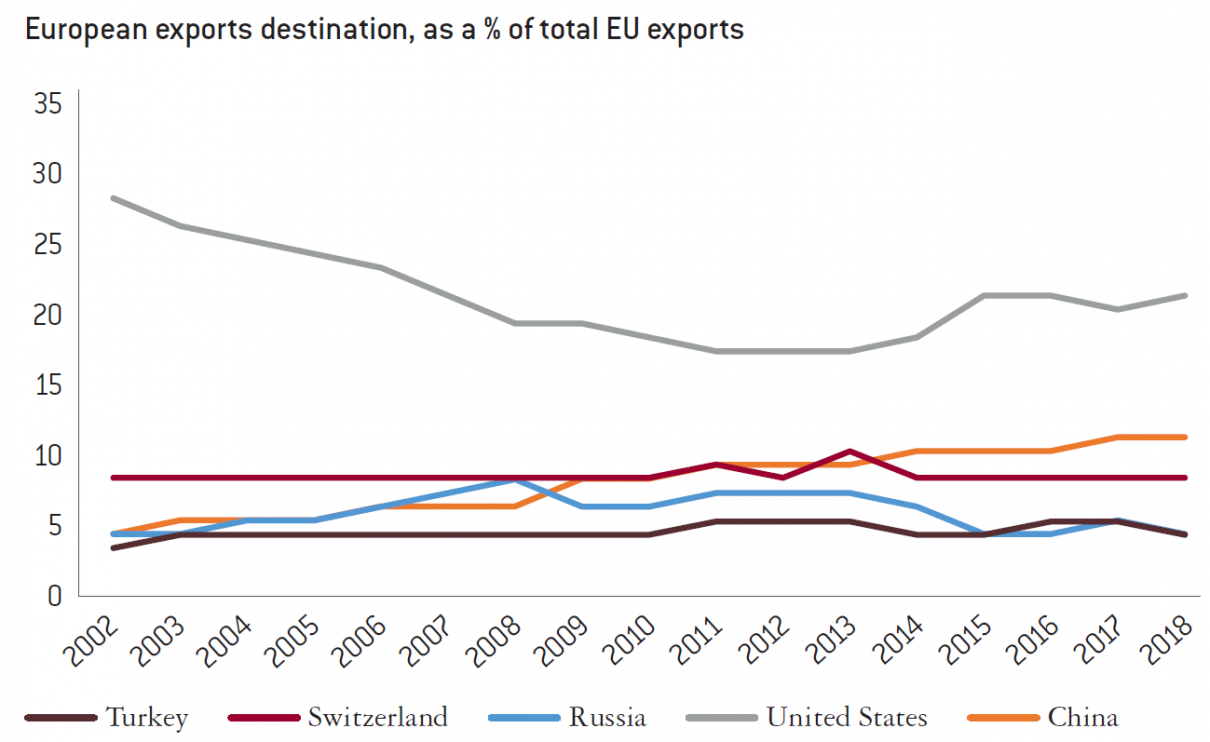

European exports destination, as a % of total EU exports

Source :

Fondation pour l’innovation politique; Eurostat data.

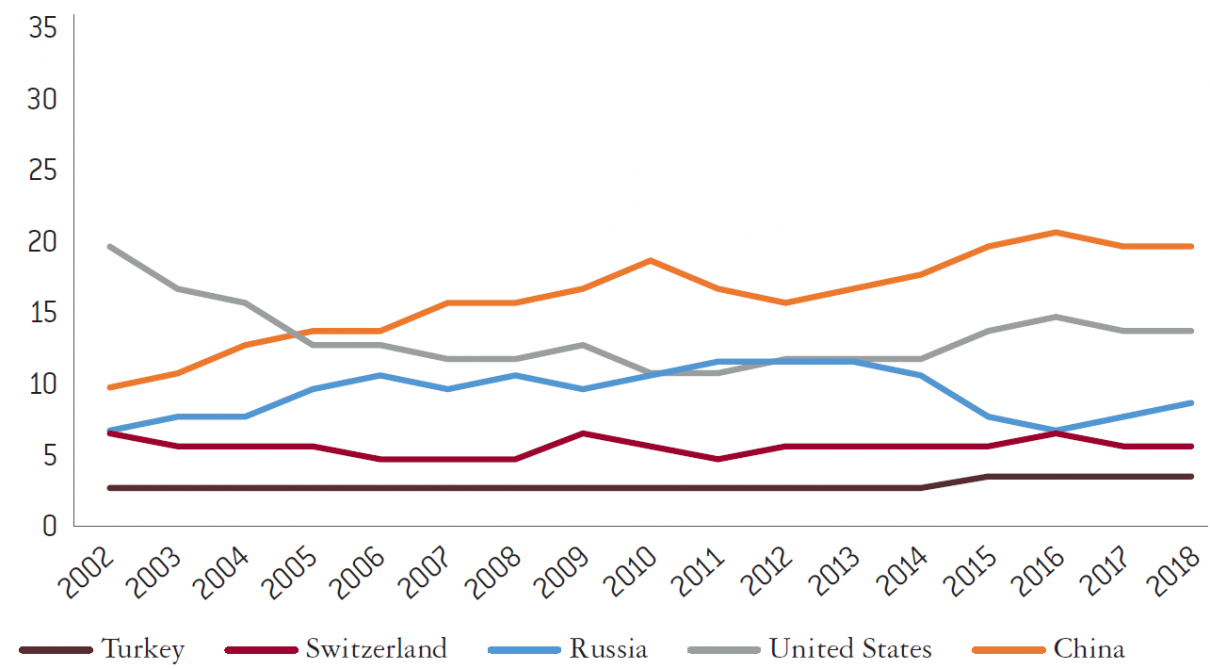

Origin of European imports, in % of total EU imports

Source :

Fondation pour l’innovation politique; Eurostat data.

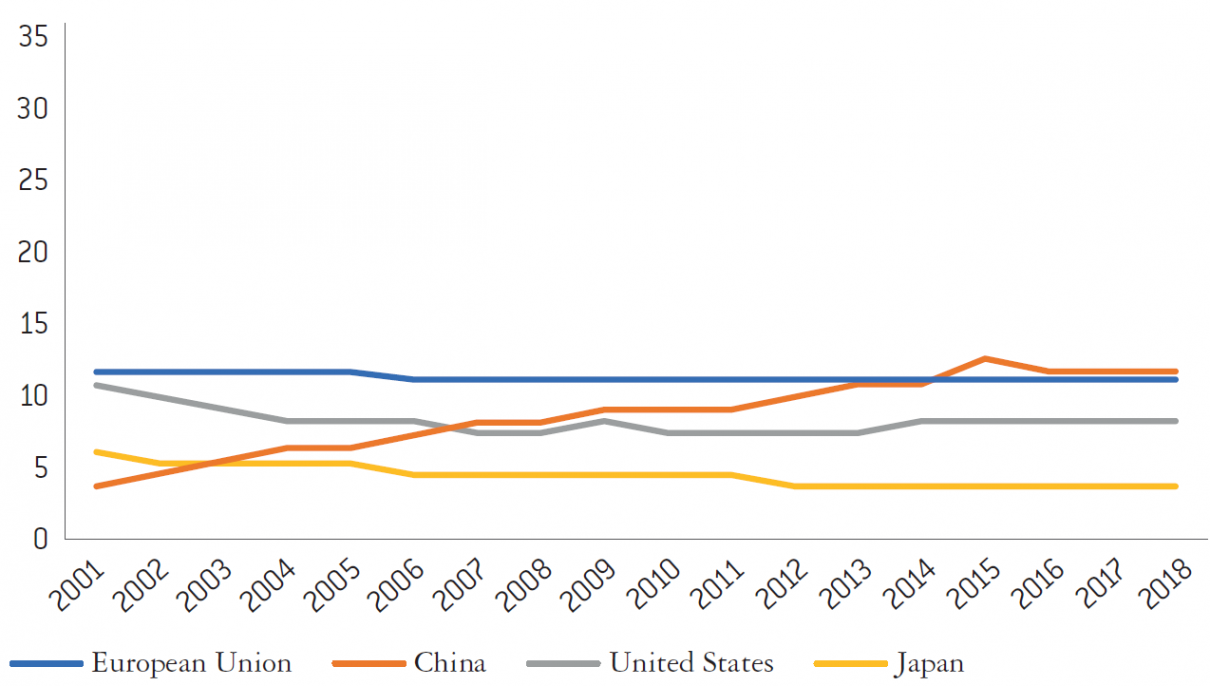

Share of domestic value added in the global value added of manufacturing industry

Source :

Fondation pour l’innovation politique; World Bank data.

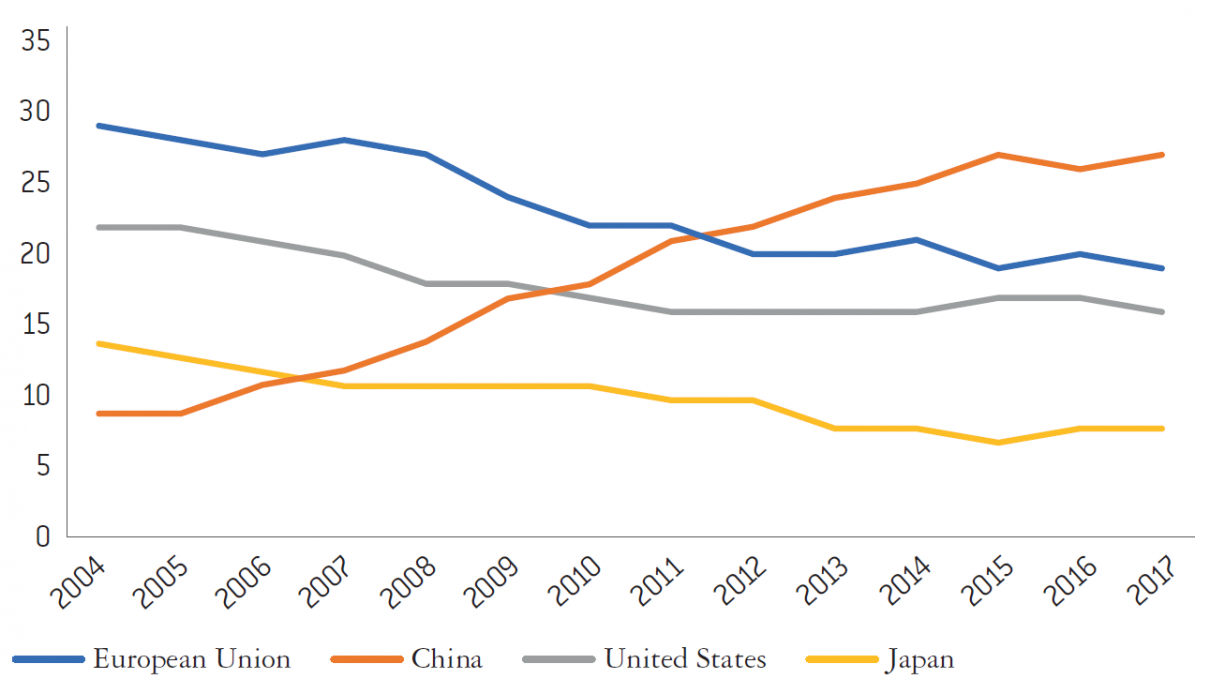

Share in value of world exports of goods (excluding intra-EU exports for the EU 28)

Source :

Fondation pour l’innovation politique; International Trade Centre data,, European Commission (Ameco).

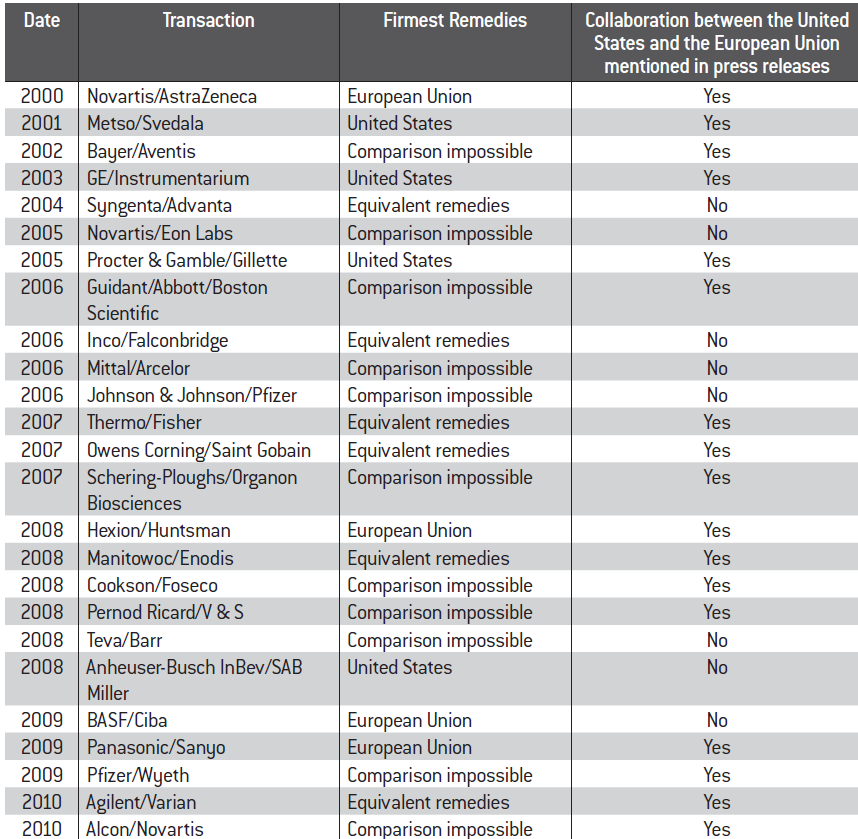

Comparisons of remedies imposed in the United States and Europe in the case of concentrations for which conditional authorisations have been granted concurrently on both sides of the Atlantic

Source :

Department of Justice, Federal Trade Commission, European Commission.

Source :

Department of Justice, Federal Trade Commission, European Commission.

No comments.